Notes to the Financial Statements

1 REPORTING ENTITY

Sri Lanka Telecom PLC (the “Company”) is a company domiciled in Sri Lanka. The address of the Company’s registered office is Lotus Road, Colombo 1. The consolidated financial statements of the Company as at and for the year ended 31 December 2013 comprise the Company and its subsidiaries (together referred to as the “Group” and individually as “Group entities”). The Group primarily is involved in providing broad portfolio of telecommunication services across Sri Lanka, In addition, the range of services provided by the Group include, inter-alia, internet services, data services, domestic and international leased circuits, broadband, satellite uplink, maritime transmission, IPTV service, directory publishing and Wi-max service .The Company is a quoted public Company which has its listing on the Colombo Stock Exchange.

2 BASIS OF PREPARATION

(a) Statement of complianceThe financial statements have been prepared in accordance with Sri Lanka Accounting Standards (SLFRS) as laid down by the Institute of Chartered Accountants of Sri Lanka(ICASL) and the requirements of the Companies Act No. 07 of 2007.

The financial statements were authorized for issue by the Board of Directors on (date)

(b) Basis of measurementThe financial statements have been prepared on the historical cost basis except for the following ; *available for sale financial assets which are measured at fair value.

The liability for defined benefit obligation recognized are actuarially valued and recognized at the present value of the defined benefit obligation.

The financial statements have been prepared on a going concern basis.

(c) Functional and presentation currencyThese financial statements are presented in Sri Lankan Rupees, which is the Company’s functional currency, and the Group’s presentation currency. All financial information presented in Sri Lankan rupees has been rounded to the nearest million.

(d) Use of estimates and judgementsThe preparation of financial statements in conformity with SLFRSs requires management to make judgments, estimates and assumptions that affect the application of accounting policies and the reported amounts of assets, liabilities, income and expenses. Actual results may differ from these estimates.

Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognized in the period in which the estimates are revised and in any future periods affected.

Information about significant areas of estimation uncertainty and judgments in applying accounting policies that have the most significant effect on the amounts recognized in the consolidated financial statements is included in notes;

- Note 13 -Property, plant and equipment

- Note 14 - Intangible Assets

- Note 20 - Trade Receivables

- Note 23 - Deferred Tax

- Note 24 - Deferred Income

- Note 26 - Employee Benefit

- Note 30 - Financial Risk Management

No changes in accounting policies have taken place during the year 2013.

3 CONSISTENCY IN ACCOUNTING POLICIES

The accounting policies set out below have been applied consistently to all periods presented in these consolidated financial statements.

(a) Basis of consolidation(i) Subsidiaries

Acquisitions on or after 1 January 2011 For acquisitions on or after 1 January 2011 , the Group measures goodwill as fair value of the consideration transferred including the recognized amount of any non controlling interest in the acquiree, less the net recognized amount ( generally fair value ) of the identifiable assets acquired and liabilities assumed, all measured as of the acquisition date. When the excess is negative, a bargain purchase gain is recognized immediately in profit or loss. The group elects on a transaction by transaction basis whether to measure non controlling interest at its fair value, or its proportionate share of the recognized amount of the identifiable net assets,at the acquisition date. Transaction costs, associated with the issue of debt or equity securities that the Group incurs in connection with a business combination are expensed as incurred.

Acquisitions prior to 1 January 2011

As part of its transition to SLFRS Group elected to restate only those business combinations that occurred on or before 31 December 2010 In respect of acquisitions prior to 31 December 2010, goodwill represents the amount recognized under the Group’s previous accounting framework, [Sri Lanka Accounting Standards “SLAS”]

(ii) Acquisitions of non-controlling interests

Acquisitions of non-controlling interests are accounted for as transactions with equity holders in their capacity as equity holders.

Therefore no goodwill is recognized as a result of such transactions.

(iii) Subsidiaries are entities controlled by the Group.

The financial statements of subsidiaries are included in the Consolidated Financial Statements from the date that control commences until the date that control ceases.

The financial statements have been prepared using uniform accounting policies for like transactions and other events in similar circumstances.

The Consolidated Financial Statements are prepared to common financial year end of 31st December.

There are no significant restrictions on the ability of Subsidiaries to transfer funds to Parent in the form of cash dividends or to repay loans and advances.

All Subsidiaries of the Group have been incorporated in Sri Lanka except SLT Hong Kong Limited (under Liquidation).

(iv) Loss of control

Upon the loss of control, the Group derecognises the assets and liabilities of the subsidiary, any non-controlling interests and the other components of equity related to the subsidiary.

Any surplus or deficit arising on the loss of control is recognized in profit or loss. If the Group retains any interest in the previous subsidiary then such interest is measured at fair value at the date that control is lost. Subsequently it is accounted for as an equity-accounted investee or in accordance with the Group’s accounting policy for financial instruments (see accounting policy v(i) depending on the level of influence retained.

(v) Transactions eliminated on consolidation

Intra-group balances and transactions, and any unrealised income and expenses arising from intra-group transactions, are eliminated in preparing the consolidated financial statements. Unrealised gains arising from transactions with equity accounted investees are eliminated against the investment to the extent of the Group’s interest in the investee. Unrealised losses are eliminated in the same way as unrealised gains, but only to the extent that there is no evidence of impairment.

(b) Foreign currency

(i) Foreign currency transactions

Transactions in foreign currencies are translated to the respective functional currencies of Group entities at exchange rates at the dates of the transactions. Monetary assets and liabilities denominated in foreign currencies at the reporting date are retranslated to the functional currency at the exchange rate at that date between amortised cost in the functional currency at the beginning of the period, adjusted for effective interest and payments during the period, and the amortised cost in foreign currency translated at the spot exchange rate at the end of the period.

Non-monetary assets and liabilities denominated in foreign currencies that are measured at fair value are retranslated into the functional currency at the spot exchange rate at the date that the fair value was determined. Foreign currency differences arising on retranslation are recognised in profit or loss, except for differences arising on the retranslation of available-for-sale equity instruments which is recognised directly in equity.

Non-monetary assets and liabilities that are measured in terms of historical cost in a foreign currency are translated using the exchange rate at the date of the transaction.

(ii) Foreign Operations

The assets and liabilities of foreign operations, including goodwill and fair value adjustments arising on acquisition, are translated into Rupees at spot exchange rates at the reporting date. The income and expenses of foreign operations are translated into Rupees at spot exchange rates at the dates of the transactions. Foreign currency differences on the translation of foreign operations are recognised in Other Comprehensive Income.

Since 1 January 2011, the Group’s date of transition to SLFRSs, such differences have been recognised in the translation reserve. When a foreign operation is disposed off, the relevant amount in the translation is transferred to profit or loss as part of the profit or loss on disposal. On the partial disposal of a subsidiary that includes a foreign operation, the relevant proportion of such cumulative amount is reattributed to non-controlling interest. In any other partial disposal of a foreign operation, the relevant proportion is reclassified to profit or loss.

Foreign exchange gains or losses arising from a monetary item receivable from or payable to a foreign operation, the settlement of which is neither planned nor likely to occur in the foreseeable future and which in substance is considered to form part of the net investment in the foreign operation, are recognised in other comprehensive income in the translation reserve.

(c) Financial assets and financial liabilities

(i) Non-derivative financial assets

The Group recognizes loans and receivables and deposits on the date that they are originated. All other financial assets (including assets designated at the fair value through profit or loss) are recognized initially on the trade date at which the Group becomes a party to the contractual provisions of the instrument. The Group derecognises a financial asset when the contractual rights to the cash flows from the asset expire, or it transfers the rights to receive the contractual cash flows on the financial asset in a transaction in which substantially all the risks and rewards of ownership of the financial assets are transferred. Any interest in transferred financial assets that is created or retained by the Group is recognized as a separate asset or liability. Financial assets and liabilities are offset and the net amount presented in the Statement of Financial Position when, and only when, the Group has a legal right to offset the amounts intends either to settle on a net basis or realize the assets and settle the liability simultaneously. The Group has the following non-derivative financial assets. Financial assets at fair value through profit or loss, held-to-maturity financial assets, loans and receivables and available-for-sale financial assets.

Financial assets at fair value through profit or loss.

A financial asset is classified at fair value through profit or loss if it is classified as held for trading or is designated as such upon initial recognition. Financial assets are designated at fair value through profit or loss if the Group manages such investments and makes purchase and sales decisions based on their fair value in accordance with the Group’s documented risk management or investment strategy. Upon initial recognition, attributable transaction costs are recognized in profit or loss as incurred. Financial assets at fair value through profit or loss are measured at fair value, and changes therein are recognized in profit or loss.

Held to-maturity financial assets.

If the Group has the positive intent and ability to hold debt securities to maturity, then such financial assets are classified as held -to -maturity. Held-to-maturity financial assets are recognized initially at fair value plus any directly attributable transactions costs. Subsequent to initial recognition held-to-maturity financial assets are measured at amortised cost using the effective interest method, less any impairment losses. Any sale or reclassification of a more than insignificant amount of held-to-maturity investments not close to their maturity would result in the reclassification of all held-to-maturity investments as available-for-sale, and prevent the Group from classifying investment securities as held-to-maturity for the current and the following two financial years.

Loans and receivables

Loans and receivables are financial assets with fixed or determinable payments that are not quoted in and active market. Such assets are recognized initially at fair value plus any directly attributable transaction costs. Subsequent to initially recognition loans and receivables are measured at amortized cost using the effective interest method, less any impairment losses.

Loans and receivables comprise cash and cash equivalents,staff loans and trade and other receivables, including related party receivables.

Cash and cash equivalents

Cash and cash equivalents comprise cash balances and call deposits with original maturities of Cash and cash equivalents comprise cash balances and call deposits with original maturities of three months or less. Bank overdrafts that are repayable on demand and form an integral part of the Group’s cash management are included as a component of cash and cash equivalents for the purpose of the statement of cash flows.

Available-for-sale financial assets

Available-for-sale financial assets are non-derivative financial assets that are designated as available-for-sale and that are not classified in any of the previous categories. The Group’s investments in equity securities and certain debt securities are classified as available-for-sale financial assets. Subsequent to initial recognition, they are measured at fair value and changes therein, other than impairment losses (see note 3(k)(i)) and foreign currency differences on available-for-sale equity instruments (see note 3(b)(i)), are recognized in other comprehensive income and presented within equity in the fair value reserve. When an investment is derecognised, the cumulative gain or loss in other comprehensive income is transferred to profit or loss.

Available-for-sale financial assets comprise debt instruments including government securities.

Fair value of Financial Instruments Carried at Amortized Cost

The table below shows the financial assets held at amortized cost.

Fair value is the amount for which an asset could be exchanged, or a liability settled, between knowledgeable, willing parties in an arm’s length transaction. The estimated

(ii) Non-derivative financial liabilities

The Group initially recognizes debt securities issued and subordinated liabilities on the date that they are originated. All other financial liabilities are trade date at which the Group becomes a party to the contractual provisions of the instrument. The Group derecognises a financial liability discharged or cancelled or expire. The Group has the following non-derivative financial liabilities :loans and borrowings, bank overdrafts, and trade and other payables. Such financial liabilities are recognized initially at fair value plus any directly attributable transaction costs. Subsequent to initial recognition these financial liabilities are measured at amortised cost using the effective interest method.

(iii) Share capital

Ordinary Share Capital

Ordinary Shares are classified as equity. Incremental costs directly attributable to the issue of ordinary shares and share options are recognized as a deduction from equity, net of any tax effects.

(d) Property, plant and equipment

(i) Recognition and measurement

(i) Recognition and measurement Items of property, plant and equipment are measured at cost less accumulated depreciation and accumulated impairment losses. As disclosed in Note 13 where property, plant and equipment of the Department of Telecommunications were transferred to Sri Lanka Telecom at a valuation performed by the Government of Sri Lanka and was used as the opening cost of fixed assets.(The cost of certain items of property, plant and equipment was determined by reference to a previous GAAP. The Group elected to apply the optional exemption to use this previous valuation as deemed cost at 1 January 2011, the date of transition to the SLFRS framework.

Cost includes expenditure that is directly attributable to the acquisition of the asset. The cost of self-constructed assets includes the cost of materials and direct labour, any other costs directly attributable to bringing the assets to a working condition for their intended use. Purchased software that is integral to the functionality of the related equipment is capitalised as part of that asset.

When parts of an item of property, plant and equipment have different useful lives, they are accounted for as separate items (major components) of property, plant and equipment.

(ii) Subsequent costs

The cost of replacing part of an item of property, plant and equipment is recognized in the carrying amount of the item if it is probable that the future economic benefits embodied within the part will flow to the Group and its cost can be measured reliably. The costs of the day-to-day servicing of property, plant and equipment are recognized in profit or loss as incurred.

(iii) Depreciation

Depreciation is calculated over the depreciable amount, which is the cost of an asset, or other amount substituted for cost, less its residual value. Depreciation is recognized in profit or loss on a straight-line basis over the estimated useful lives of each part of an item of property, plant and equipment. In the year of acquisition depreciation is computed on proportionate basis from the month the asset is put in to use and no depreciation will be charged to the month in which the particular asset was disposed. Leased assets are depreciated over the shorter of the lease term and their useful lives unless it is reasonably certain that the Group will obtain ownership by the end of the lease term. Land is not depreciated.

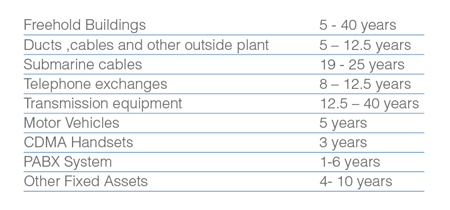

Depreciation method,useful lives and residual values are reviewed at each reporting date and adjusted if appropriate. Estimated useful lives in respect of certain items of property,plant and equipment were revised from 1 January 2011.

The estimated useful lives for the assets are as follows:

(iv) Capital Work-in-Progress

Capital work-in-progress is stated at cost. These are expenses of a capital nature directly incurred in the construction of buildings, major plant and machinery and system development, awaiting capitalization.

(v) Derecognition

The carrying amount of an item of Property, Plant & Equipment is derecognised on disposal. Gains and losses on disposal of an item of property, plant and equipment are determined by comparing the proceeds from disposal with the carrying amount of property, plant and equipment, and are recognized net within “other income” in profit or loss.

When replacement costs are recognized in the carrying amount of an item of Property, Plant and Equipment, the remaining carrying amount of the replaced part is derecognised. Major inspection costs are capitalized. At each such capitalization, the remaining carrying amount of the previous cost of inspections is derecognised.

(e) Intangible assets

(i) Goodwill

Goodwill arises on the acquisition of subsidiaries. Goodwill that arises upon the acquisition of subsidiaries is included in intangible assets. For measurement of goodwill at initial recognition,see note 3(a)(i) The Group has elected to not apply SLFRS 3 retrospectively to past business combinations. Therefore, in respect of acquisitions occurred prior to 1 January 2011 goodwill represents the amount recorded under previous GAAP.

Subsequent measurement

Goodwill is measured at cost less accumulated impairment losses.

(ii) Other intangible assets

Other intangible assets that are acquired by the Group, which have finite useful lives, are measured at cost less accumulated amortisation and accumulated impairment losses.

(iii) Licenses

Separately acquired licences are shown at historical cost. Expenditures on license fees that is deemed to benefit or relate to more than one financial year is classified as license fee and is being amortized over the License period on a straight line basis.

(iv) Subsequent expenditure

Subsequent expenditure is capitalized only when it increases the future economic benefits embodied in the specific asset to which it relates. All other expenditure, including expenditure on internally generated goodwill is recognized in profit or loss as incurred.

(v) Amortisation

Amortisation is recognized in profit or loss on a straight-line basis over the estimated useful lives of intangible assets, other than goodwill, from the date that they are available for use. The estimated useful lives for the current and comparative periods are as follows: Software 3- 5 years

An impairment loss in respect of goodwill is not reversed. In respect of other assets, impairment losses recognized in prior periods are assessed at each reporting date for any indications that the loss has decreased or no longer exists. An impairment loss is reversed if there has been a change in the estimates used to determine the recoverable amount. An impairment loss is reversed only to the extent that the asset’s carrying amount does not exceed the carrying amount that would have been determined, net of depreciation or amortisation, if no impairment loss had been recognized.

(ii) Financial assets

A financial asset not carried at fair value through profit or loss is assessed at each reporting date to determine whether there is objective evidence that it is impaired. A financial asset is impaired if objective evidence indicates that a loss event has occurred after the initial recognition of the asset, and that the loss event had a negative effect on the estimated future cash flows of that can be estimated reliably. Objective evidence that financial assets are impaired can include default or delinquency by a debtor,restructuring of an amount due to the Group on terms that the Group would not consider otherwise, indications that a debtor or issuer will enter bankruptcy, or the disappearance of an active market for a security.

The Group considers evidence of impairment for receivables and held-to-maturity investment securities at both a specific asset and collective level. All individually significant receivables and held-to-maturity investment securities are assessed for specific impairment. All individually significant receivables and held-to-maturity investment securities found not to be specifically impaired are then collectively assessed for any impairment that has been incurred but not yet identified.

In assessing collective impairment the Group uses historical trends of the probability of default, timing of recoveries and the amount of loss incurred, adjusted for management’s judgment as to whether current economic and credit conditions are such that the actual losses are likely to be greater or less than suggested by historical trends. An impairment loss in respect of a financial asset measured at amortised cost is calculated as the difference between its carrying amount and the present value of the estimated future cash flows discounted at the asset’s original effective interest rate. Losses are recognized in profit or loss and reflected in an allowance account against receivables.

Impairment losses on available-for-sale investment securities are recognized by transferring the cumulative loss that has been recognized in other comprehensive income, and presented in the fair value reserve in equity, to profit or loss. The cumulative loss that is removed from other comprehensive income and recognized in profit or loss is the difference between the acquisition cost, net of any principal repayment and amortisation, and the current fair value, less any impairment loss previously recognized in profit or loss. Changes in impairment provisions attributable to time value are reflected as a component of interest income.

(i) Government Grants

Government grants are recognized initially at fair value when there is reasonable assurance that they will be received and the Group will comply with the conditions associated with the grant. Grants that compensate the Group for expenses incurred are recognized in profit or loss as other income on a systematic basis in the same periods in which the expenses are recognized. Grants that compensate the Group for the cost of an asset are recognized in profit or loss on a systematic basis over the useful life of the asset.

(j) Employee benefits

(i) Defined contribution plans

A defined contribution plan is a post-employment benefit plan under which contributions are made into a separate fund and the entity will have no legal or constructive obligation to pay further amounts. Obligations for contributions to defined contribution plan are recognized as an employee benefit expense in profit or loss in the periods during services is rendered by employees. Prepaid contributions are recognized as an asset to the extent that a cash refund or a reduction in future payments is available.

Employee Provident Fund

All employees of the Company are members of the Sri Lanka Telecom Provident Fund to which the Company contributes 15% of such employees’ basic salary and allowances.

All employees of subsidiaries of the Group except for SLT Hong Kong Limited and Sri Lanka Telecom (Services) Limited are members of Employees’ Provident Fund (EPF), to which respective subsidiaries contribute 12% of such employees’ basic salary and allowances. Employees of SLT Services (Private) Ltd are members of Employees’ Provident Fund (EPF), where the company contribute 15% of such employees’ basic salary and allowances.

Employee Trust Fund

The Company and other subsidiaries contribute 3% of the salary of each employee to the Employees’ Trust Fund.

A defined benefit plan is a post-employment benefit plan other than a defined contribution plan. The Group’s net obligation in respect of defined benefit plans is calculated separately for each plan by estimating the amount of future benefit that employees have earned in return for their service in the current and prior periods; that benefit is discounted to determine its present value. The valuation is performed annually by a qualified actuary using the projected unit credit method. When the valuation results in a benefit to the Group, the recognized asset is limited to the total of any unrecognised past service costs and the present value of economic benefits available in the form of any future refunds from the plan or reductions in future contributions to the plan. An economic benefit is available to the Group if it is realizable during the life of the plan, or on settlement of the plan liabilities.

When the benefits of a plan are improved, the portion of the increased benefit relating to past service by employees is recognized in profit or loss on a straight-line basis over the average period until the benefits become vested. To the extent that the benefits vest immediately, the expense is recognized immediately in profit or loss.

(iii) Termination benefits

Termination benefits are recognized as an expense when the Group is demonstrably committed, without realistic possibility of withdrawal, to a formal detailed plan to either terminate employment before the normal retirement date, or to provide termination benefits as a result of an offer made to encourage voluntary redundancy. Termination benefits for voluntary redundancies are recognized as an expense if the Group has made an offer of voluntary redundancy, it is probable that the offer will be accepted, and the number of acceptances can be estimated reliably.

(iv) Short-term benefits

Short-term employee benefit obligations are measured on an undiscounted basis and are expensed as the related service is provided.

(k) Provisions

A provision is recognized if, as a result of a past event, the Group has a present legal or constructive obligation that can be estimated reliably, and it is probable that an outflow of economic benefits will be required to settle the obligation. Provisions are determined by discounting expected future cash flows at a pre-tax rate that reflects current market assessment of the time value of money and the risk specific to the liability. Unwinding of discount is recognized as finance cost.

(l) Revenue

Revenue from services rendered in the course of ordinary activities is measured at fair value of the consideration received or receivable net of trade discounts ,volume rebates and after eliminating the sales within the Group.

Revenue is recognized when persuasive evidence exist , usually in the form of an executed sales agreement, that the significant risks and rewards of ownership have been transferred to the customer, recovery of the consideration is probable and the amount of revenue can be measured reliably.

If it is probable that discounts will be granted and the amount can be measured reliably, then the discount is recognized as a reduction of revenue as the sales are recognized.

The revenue is recognized as follows:

(i) Domestic and international call revenue, rental income

Revenue for call time usage by customers is recognized as revenue as services are performed on accrual basis. Fixed rental is recognized as income on a monthly basis in relation to the period of services rendered.

(ii) Revenue from other network operators and international settlements

The revenue received from other network operators, local and international, for the use of the Group’s telecommunication network are recognized, net of taxes, based on usage taking the traffic minutes/per second rates stipulated in the relevant agreements and regulations and based on the terms of the lease agreements for fixed rentals. Revenue arising from the interconnection of voice and data traffic between other telecommunications operators is recognized at the time of transit across the group’s network and presented on gross basis. The relevant revenue accrued is recognized under income in the Statement of comprehensive income and interconnection expenses recognized under operating costs in the statement of comprehensive income.

(iii) Revenue from broadband

Revenue from Data services and IPTV services is recognized on usage and the fixed rental on a monthly basis when it is earned net of taxes, rebates and discounts.

(iv) Revenue from other telephony services

The revenue from other telephony services are recognized on an accrual basis based on fixed rental contracts entered between the Group and subscribers.

(v) Connection fees

The connection fees relating to Public Switched Telephone Network (PSTN) are deferred over a period of 15 years. Revenue is recognized on an annual basis irrespective of the date of connection.

The connection fees relating to Code Divisional Multiple Access (CDMA) connections are recognized as revenue at the point the connection is activated.

(vi) Service Agreements revenue

Capacity contracts which do not convey the right to use a specified capacity in an identified fibre cable are accounted as service arrangements. Revenues from capacity contracts under service arrangements are recognized on a straight line basis over the period of the contracts. Amounts received in advance for any services are recorded as deferred revenue. In the event that a customer terminates an IRU prior to the expiry of the contract and releases the Company from the obligation to provide future services, the remaining unamortized deferred revenue is recognized in the period the contract is terminated.

(vii) Prepaid Card revenue

Revenue from the sale of prepaid credit on CDMA, Internet is deferred until such time as the customer uses the call time, downloadable quota or the credit expires.

(viii) Equipment Sales

Revenue from sale of equipment is recognized, net of taxes, once the equipment is delivered.

(ix) Sales of services

Revenue from publication sales relating to advertising revenue is recognized on publishing the advertisement on the telephone directory and a copy delivered to the subscriber on a percentage of completion method.

(m) Expenditure

The expenses are recognized on an accrual basis. All expenses incurred in the ordinary course of business and in maintaining property, plant and equipment in a state of efficiency is charged against income in arriving at the profit for the year.

(n) Lease payments

Payments made under operating leases are recognized in profit or loss on a straight-line basis over the term of the lease. Lease incentives received are recognized as an integral part of the total lease expense, over the term of the lease.

Minimum lease payments made under finance leases are apportioned between the finance expense and the reduction of the outstanding liability. The finance expense is allocated to each period during the lease term so as to produce a constant periodic rate of interest on the remaining balance of the liability.

Contingent lease payments are accounted for by revising the minimum lease payments over the remaining term of the lease when the lease adjustment is confirmed. Determining whether an arrangement contains a lease.

At inception of an arrangement, the Group determines whether such an arrangement is or contains a lease. A specific asset is the subject of a lease if fulfilment of the arrangement is dependent on the use of that specific asset. An arrangement conveys the right to use the asset if the arrangement conveys to the Group the right to control the use of the underlying asset.

(o) Finance income and expenses

Finance income comprises interest income on funds invested (including available for sale financial assets) , dividend income, gains on the disposal of available for sale financial assets. Interest income is recognized as it accrues in profit or loss on the date that the Group’s right to receive payment is established, which in the case of quoted securities is normally the ex-dividend date.

Dividend income is recognized in profit or loss on the date that the Group’s right to receive payment is established, which in the case of quoted securities is the ex-dividend date.

Finance expenses comprise interest expense on borrowings.

Foreign currency gains and losses are reported on a net basis, as either finance income or finance cost depending on whether foreign currency movements are in a net gain or net loss position.

(p) Income tax

Income tax expense comprises current and deferred tax. Income tax expense is recognized in profit or loss except to the extent that it relates to items recognized directly in equity, in which case it is recognized in equity or other comprehensive income.

(i) Current Taxation

Current tax is the expected tax payable on the taxable income for the year, using tax rates enacted or substantively enacted at the reporting date, and any adjustment to tax payable in respect of previous years. Current tax payable also includes any tax liability arising from the declaration of dividend.

(ii) Deferred Taxation

Deferred tax is recognized in respect temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for taxation purposes. Deferred tax is not recognized for the following temporary differences: the initial recognition of assets or liabilities in a transaction that is not a business combination and that affects neither accounting nor taxable profit or loss, and differences relating to investments in subsidiaries to the extent that it is probable that they will not reverse in the foreseeable future. In addition, deferred tax is not recognized for taxable temporary differences arising on the initial recognition of goodwill. Deferred tax is measured at the tax rates that are expected to be applied to temporary differences when they reverse, based on the laws that have been enacted or substantively enacted by the reporting date. Deferred tax assets and liabilities are offset if there is a legally enforceable right to offset current tax liabilities and assets, and they relate to income taxes levied by the same tax authority on the same taxable entity, or on different tax entities, but they intend to settle current tax liabilities and assets on a net basis or their tax assets and liabilities will be realised simultaneously.

A deferred tax asset is recognized to the extent that it is probable that future taxable profits will be available against which the temporary difference can be utilised. Deferred tax assets are reviewed at each reporting date and are reduced to the extent that it is no longer probable that the related tax benefit will be realised.

(iii) Economic Service Charge (ESC)

ESC is payable on the liable turnover at specified rates. As per the provision of the Economic Service Charge Act No. 13 of 2006 and subsequent amendments thereto, ESC is deductible from the income tax liability. Any unclaimed payment can be carried forward and set off against the income tax payable as per the relevant provision in the Act.

(q) Earnings per share

The Group presents basic and diluted earnings per share (EPS) data for its ordinary shares. Basic EPS is calculated by dividing the profit or loss attributable to ordinary shareholders of the Company by the weighted average number of ordinary shares outstanding during the period. Diluted EPS is determined by adjusting the profit or loss attributable to ordinary shareholders and the weighted average number of ordinary shares outstanding for the effects of all dilutive potential ordinary shares.

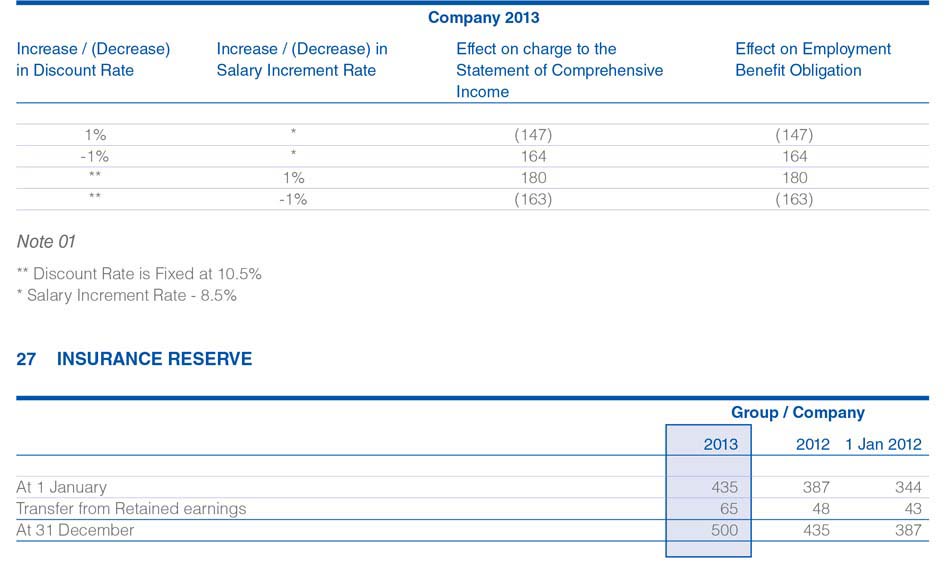

(r) Insurance reserve

The Company transfers annually from the retained earnings an amount equal to 0.1% of additions to property, plant and equipment to an insurance reserve. An equal amount is invested in a sinking fund to meet any funding requirements for potential losses from uninsured property, plant and equipment. The insurance reserve is maintained to recover any losses arising from damage to property, plant and equipment, except for motor vehicles, that are not insured with a third party insurer.

(s) Dividend distribution

Dividend distribution to the Company’s shareholders is recognized as a liability in the Group’s financial statements in the period in which the dividends are approved by the Company’s shareholders.

Provision for final dividends is recognized at the time the dividend recommended and declared by the Board of Directors, is approved by the shareholders.

(t) Comparatives

Except when a standard permits or requires otherwise, comparative information is disclosed in respect of the previous period. Where the presentation or classification of items in the financial statements are amended, comparative amounts are reclassified unless it is impracticable.

(u) Capital management

The Board’s policy is to maintain a strong capital base so as to maintain investor, creditor and market confidence and to sustain future development of the business. Capital consists of stated capital, reserves and non-controlling interests of the Group. The Board of Directors monitors the return on capital as well as the level of dividends to ordinary shareholders.

The Group’s objectives when managing capital are to safeguard the Group’s ability to continue as a going concern in order to provide returns for shareholders and benefits for other stakeholders and to maintain an optimal capital structure to reduce the cost of capital.

In order to maintain or adjust the capital structure, the Group may adjust the amount of dividends paid to shareholders, return capital to shareholders, issue new shares or sell assets to reduce debt.

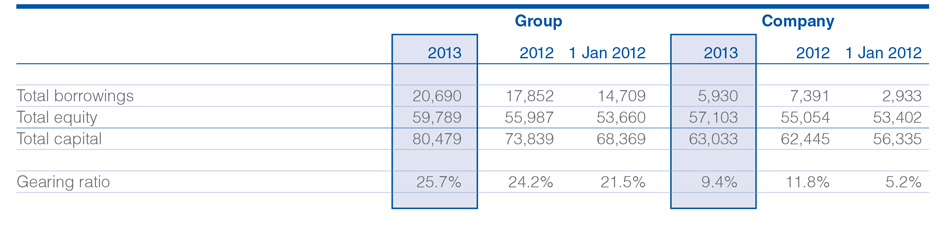

During 2013, the Group’s strategy, which was unchanged from 2010, was to maintain the gearing ratio below 26 %. The gearing ratios at 31 December 2013, 2012 and 01 January 2012 were as follows:

Risk Management Framework

The Board of Directors has overall responsibility for the establishment and oversight of the Group’s risk management framework.

The Group’s risk management processes are established to identify and analyse the risks faced by the Group, to set appropriate risk limits and controls, and to monitor risks and adherence to limits. Risk management systems are reviewed regularly to reflect changes in market conditions and the Group’s activities.

The Audit Committee oversees how management monitors compliance with the Group’s risk management processes /guidelines and procedures, and reviews the adequacy of the risk management framework in relation to the risks . The Audit Committees are assisted in its oversight role by Internal Audit. Internal Audit undertakes both regular and ad hoc reviews of risk management controls and procedures, the results of which are reported to the Audit Committee.

(v) New standards and interpretations not yet adopted

A number of new standards, amendments to standards and interpretations are effective for annual periods beginning after 1 January 2012, and have not been applied in preparing these consolidated financial statements. Those which may be relevant to the Group are set out below. The Group does not plan to adopt these standards early.

(i) SLFRS 9 Financial Instruments

SLFRS 9 (2009) introduces new requirements for the classification and measurement of financial assets. Under SLFRS 9 (2009), financial assets are classified and measured based on the business model in which they are held and the characteristics of their contractual cash flows. SLFRS 9 (2010) introduces additions relating to financial liabilities. The IASB currently has an active project to make limited amendments to the classification and measurement requirements of SLFRS 9 and add new requirements to address the impairment of financial assets and hedge accounting.

SLFRS 9 is effective for annual periods beginning on or after 1 January 2015 with early adoption permitted. The adoption of SLFRS 9 (2010) is expected to have an impact on the Group’s financial assets, but not any impact on the Group’s financial liabilities.

(ii) SLFRS 10 Consolidated Financial Statements, SLFRS 11 Joint Arrangements, SLFRS 12 Disclosure of Interests in Other Entities (2011)

SLFRS 10 introduces a single control model to determine whether an investee should be consolidated. As a result, the Group may need to change its consolidation conclusion in respect of its investees, which may lead to changes in the current accounting for these investees.

Under SLFRS 11, the structure of the joint arrangement, although still an important consideration, is no longer the main factor in determining the type of joint arrangement and therefore the subsequent accounting.

SLFRS 12 brings together into a single standard all the disclosure requirements about an entity’s interests in subsidiaries, joint arrangements, associates and unconsolidated structured entities. The Group is currently assessing the disclosure requirements for interests in subsidiaries, interests in joint arrangements and associates and unconsolidated structured entities in comparison with the existing disclosures. SLFRS 12 requires the disclosure of information about the nature, risks and financial effects of these interests.

These standards are effective for annual periods beginning on or after 1 January 2014 with early adoption permitted.

(iii) SLFRS 13 Fair Value Measurement (2011)

SLFRS 13 provides a single source of guidance on how fair value is measured, and replaces the fair value measurement guidance that is currently dispersed throughout SLFRS. Subject to limited exceptions, SLFRS 13 is applied when fair value measurements or disclosures are required or permitted by other SLFRSs. The Group is currently reviewing its methodologies in determining fair values. SLFRS 13 is effective for annual periods beginning on or after 1 January 2014 with early adoption permitted.

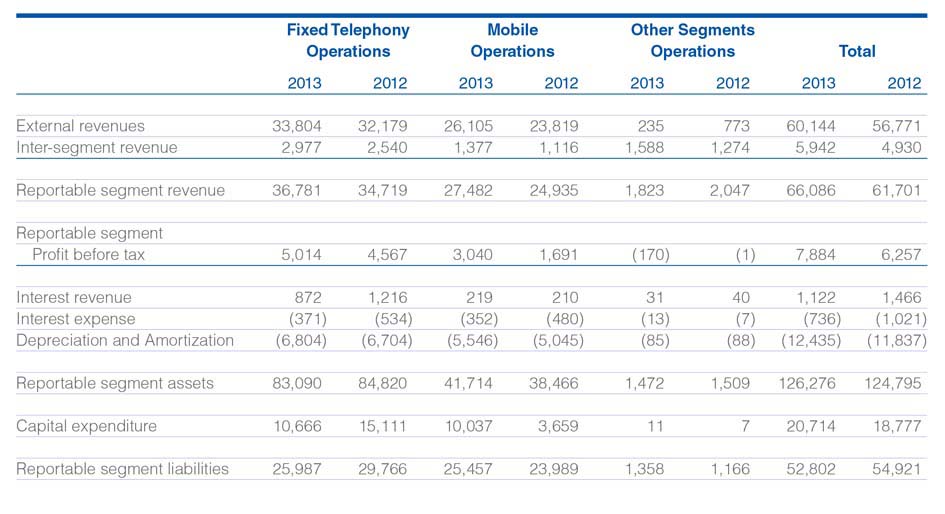

4. OPERATING SEGMENTS

The Group has three reportable segments, as described below, which are the Group’s strategic divisions. The strategic divisions offer different products and services, and are managed separately because they require different technology and marketing strategies. For each of the strategic divisions, the board of Directors (the Chief Operating Decision Maker - CODM) reviews internal management reports on at least quarterly basis. The following summary describes the operations in each of the Group’s reportable segments.

- Fixed Telephony operations includes supply of fixed telecommunication services.

- Mobile Telephony operations includes supply of mobile telecommunication services.

- Other Segment operations includes Directory publication & support services. None of these segments meet the quantitative thresholds for determining reportable Segments in 2013 or 2012.

Information regarding the results of each reportable segment is included below. Performance is measured based on segment profit before tax, as included in the internal management reports that are reviewed by the Board of Directors (BOD). Segment profit is used to measure performance as management believes that such information is the most relevant in evaluating the results of certain segments relative to other entities that operate within these industries.

Information about reportable segments.

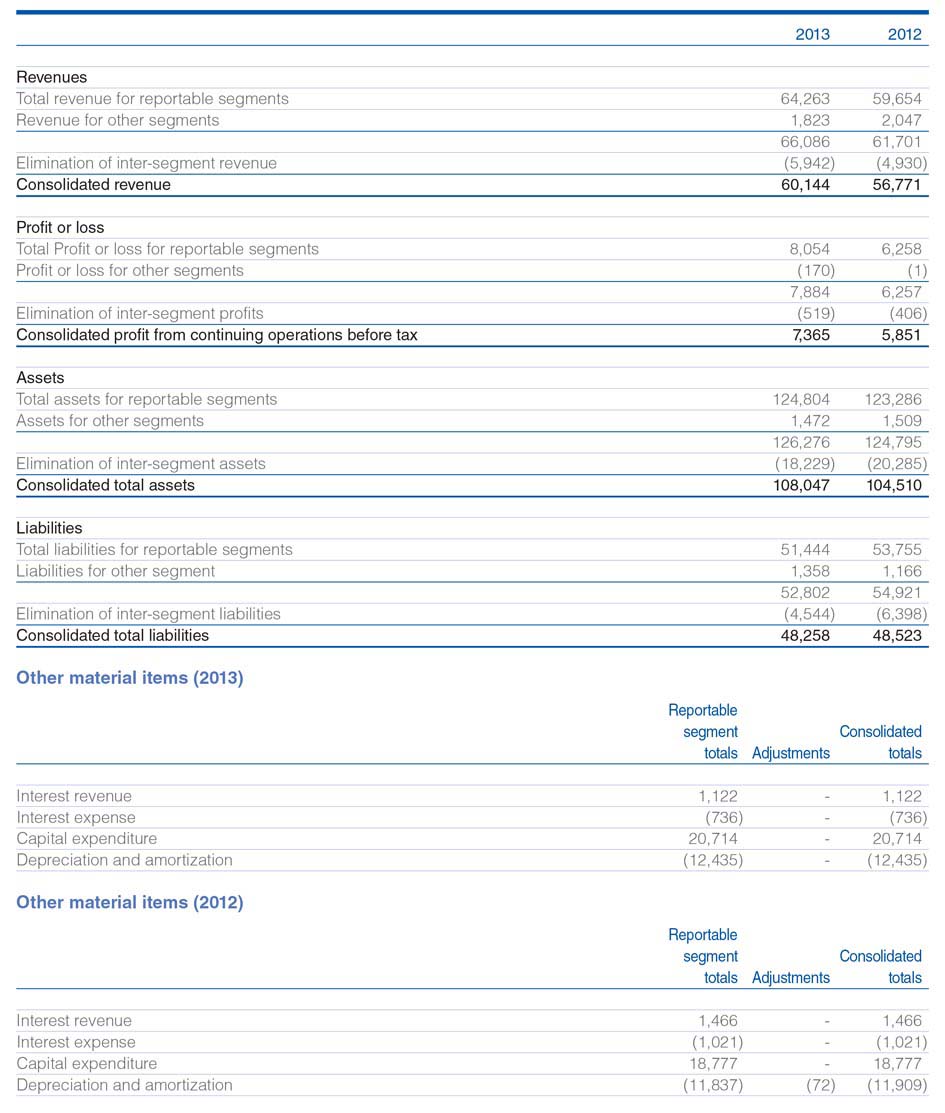

Reconciliations of reportable segment revenues, profit or loss, assets and liabilities, and other material items

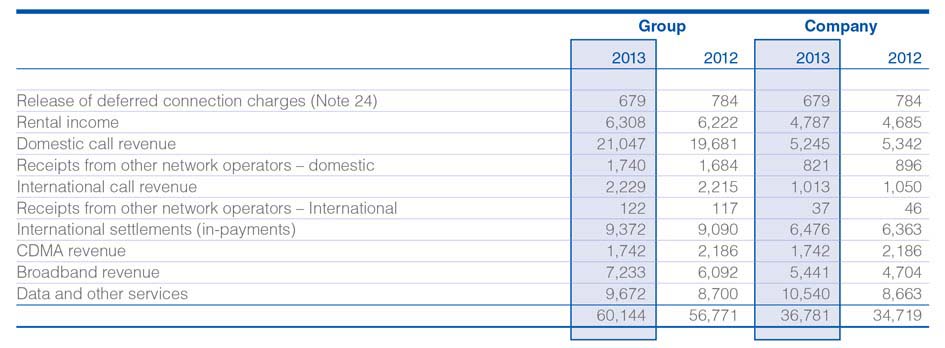

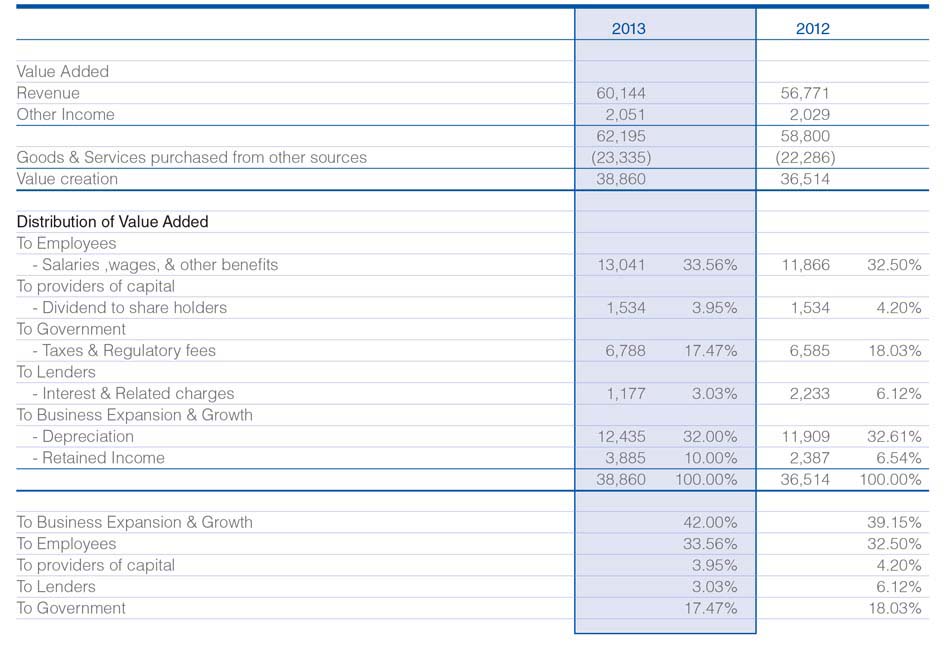

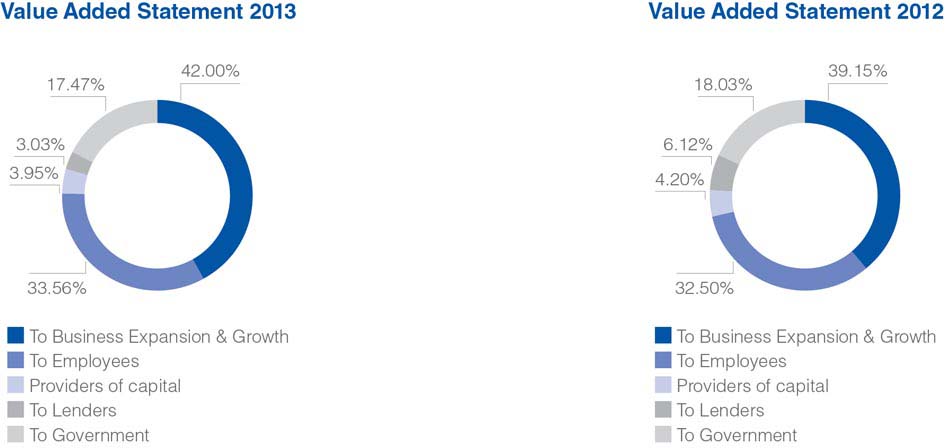

5 REVENUE

The significant categories under which revenue is recognized are as follows:

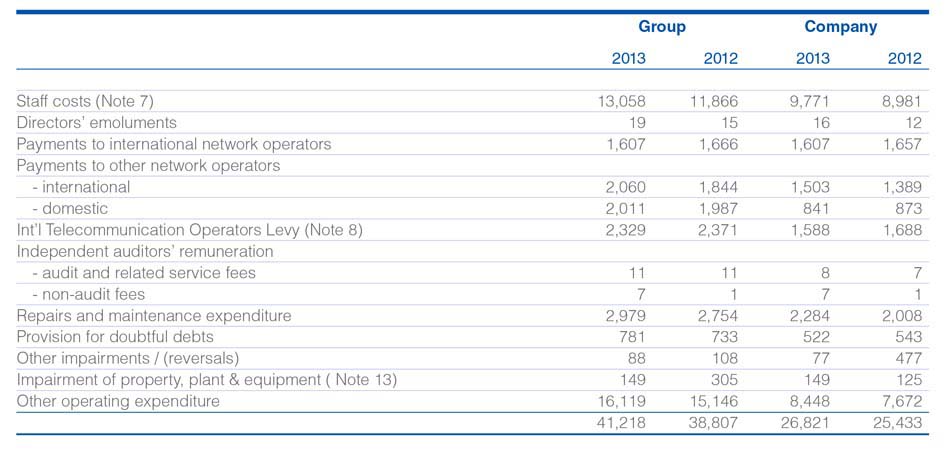

6 OPERATING COSTS

The following items have been included in arriving at operating profit before depreciation and amortisation:

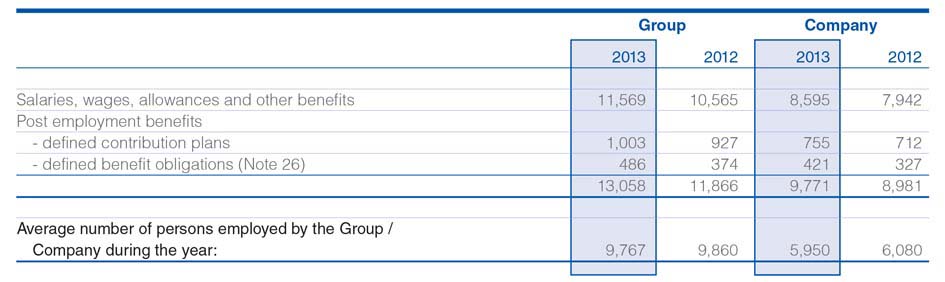

7 STAFF COSTS

8 REFUNDS ON TELECOMMUNICATION DEVELOPMENT CHARGE (TDC)

In accordance with the Finance Act.No. 11 of 2004, all Telecommunication Gateway Operators are required to pay a levy defined as the Telecommunication Development Charge (TDC) to the Government of Sri Lanka, based on international call minutes terminated in the country. This levy was made effective from 03 March 2003, where initially the levy was defined in such a way that Operators were allowed to claim the 2/3rd of TDC against the cost of network development charges

The first revision to this rate was introduced with effect from 15 July, 2010 with a TDC rate change from US cents 3.80 to US cents 1.50. Through the same revision the disbursement process was removed from the regulation. The revised rates prevailed until such time the rate was again revised to US cents 3.0 per minute with effect from 01 January, 2012 in accordance with the Budget Proposal for year 2012.

The total amount of the levy payable by the Group and Company for the period from 01 January to 31 December, 2013 was estimated at Rs. 2,329 million ( 2012 – Rs. 2,371 million) and Rs. 1,588 million (2012 – Rs.1,688 million) respectively and has been recognized as expenses in the current financial year. The corresponding liability net of payments has been recognized in the Statement of Financial Position.

The Telecommunication Regulatory Commission (TRC) refunded Rs.367 million as claims for the period from 01 April 2008 to 31 March 2009 during the year 2013. The TDC refund is accounted for on cash basis when the payment is received from the TRC. For the period 1 April 2009 to 14 July 2010, for which the disbursement regulation is effective, claims amounting to Rs.948 million was submitted to the TRC for which no refunds were received.

9 INTEREST EXPENSE AND FINANCE COSTS

(a) Interest cost of the company Rs 348 million (2012-Rs 519 million) relates to the LKR loans and USD syndicated loans. Interest cost of the group related to LKR loans and USD syndicated loans.

(b) Other charges mainly include interest cost of finance leases and overdraft facilities.

9.a Foreign Exchange (Loss) /Gain

(a) Foreign currency (loss) or gain of the company mainly includes,

- i. Exchange gain of Rs.220 million (2012 - Rs. 1,101 million) arising from revaluation of the fixed deposits and bank balances maintained in USD

- ii. Exchange loss of Rs 31 million on payment to foreign suppliers (2012 - gain Rs. 5 million)

- iii. Exchange loss of Rs.171 million (2012 - Rs. 1,031 million) arising from revaluation of USD syndicated loan

(b) Foreign currency (loss) or gain of the group mainly includes,

- i. Exchange gain of Rs.220 million (2012 - of Rs. 1,339 million) arising from revaluation of the fixed deposits and bank balances maintained in USD

- ii. Exchange loss of Rs. 391 million on payment to foreign suppliers (2012 - Rs. 1,028 million)

- iii. Exchange loss of Rs. 270 million (2012 - Rs.1,523 million) arising from revaluation of USD syndicated loan and other term loans.

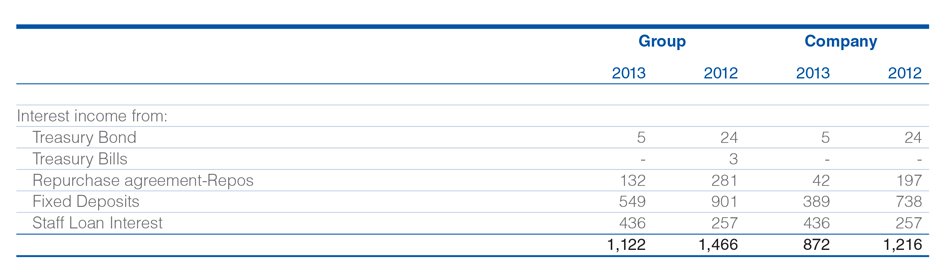

10 INTEREST INCOME

The interest income on bank deposits and Government Securities reflect the prevailing rates on the date of respective investments.

(a) The weighted average interest rates on bank deposits in LKR and USD were 15.28% (2012 - 12.80%) and 5.28 % (2012 - 5.42%) respectively.

(b) The weighted average interest rates on investments in Government Securities were 8.64% (2012 - 9.81%)

(c) The weighted average interest rates on staff loans are between 11.50% and 20% (2012 - 11.5% and 20%).

(d) According to the section 137 of the Inland Revenue Act No 10. of 2006, any person who derives income from the secondary market transactions in government securities is entitled to a notional tax credit in relation to the tax payable by such person. Notional tax credit would be determined by grossing up of the income from the secondary market transactions to an amount equal to 1/9 of same and credit to be afforded for a like sum. Accordingly , company has accounted for Rs.5 Million as notional tax credit for the year 2013. (2012 Rs 23 Million)

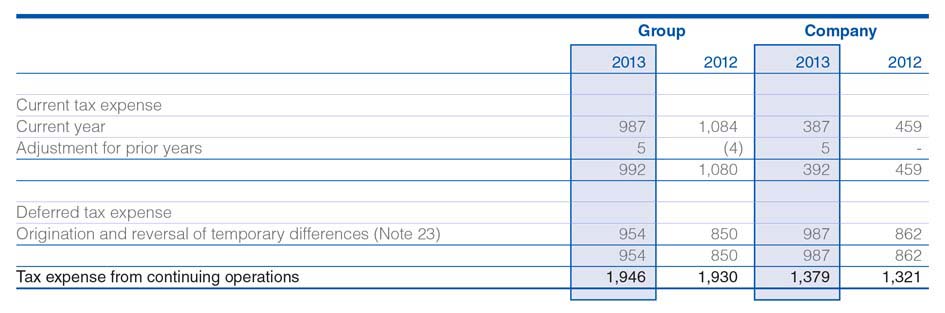

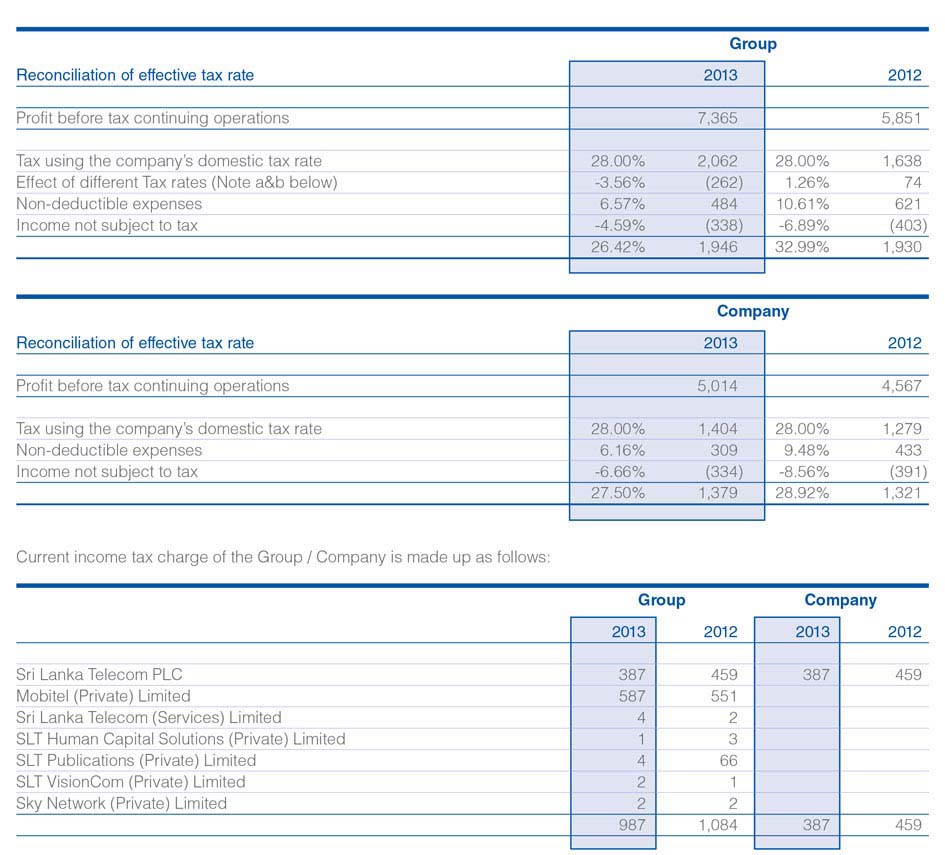

11 INCOME TAX EXPENSES

Tax recognized in profit or loss

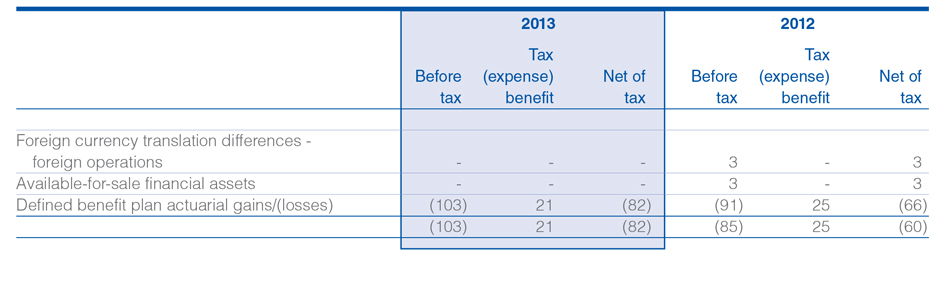

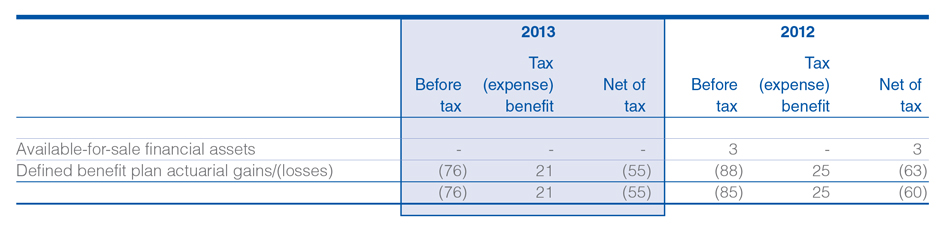

Tax recognized in other comprehensive income -Group

Tax recognized in other comprehensive income -Company

(a) Pursuant to agreements dated 15 January 1993 and 26 February 2001 entered into with the Board of Investment of Sri Lanka under Section 17 of the Board of Investment Act No. 4 of 1978, 15 years tax exemption period granted to Mobitel (Private) Limited expired on 30 June 2009 and as per the agreement, Mobitel (Private) Limited opted for the turnover based tax option in which 2% was charged on the turnover for a further period of 15 years commencing from 1 July 2009.

(b) As per the amendment to Inland Revenue Act no 22 of 2011, for the year of assessment 2013/2014, SLT Human Capital Solutions (Pvt) Limited is liable for income taxes at the rate of 10% on their taxable income.

(C) As per the agreement with the Board of Investment of Sri Lanka (BOI) dated 19 November 2009 under Section 17 of BOI Act No.4 of 1978 the Sky Network (Private) Ltd is exempt from income tax for a period of 6 years. For the above purpose the year of assessment shall be reckoned from the year in which the company commences to make profits or any year of assessment not later than two years reckoned from the date of on which the Company commences commercial operation, whichever is earlier as may be specified in a certificate issued by the Board. In view of the above the Company is not liable to income tax on business profit. The Current tax wholly consists of tax on interest income.

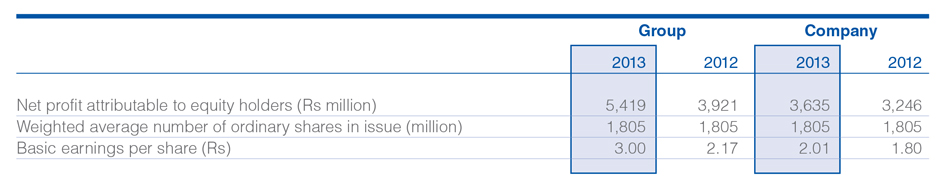

12 EARNINGS PER SHARE

The basic earnings per share is calculated by dividing the net profit attributable to equity holders by the weighted average number of ordinary shares in issue during the year.

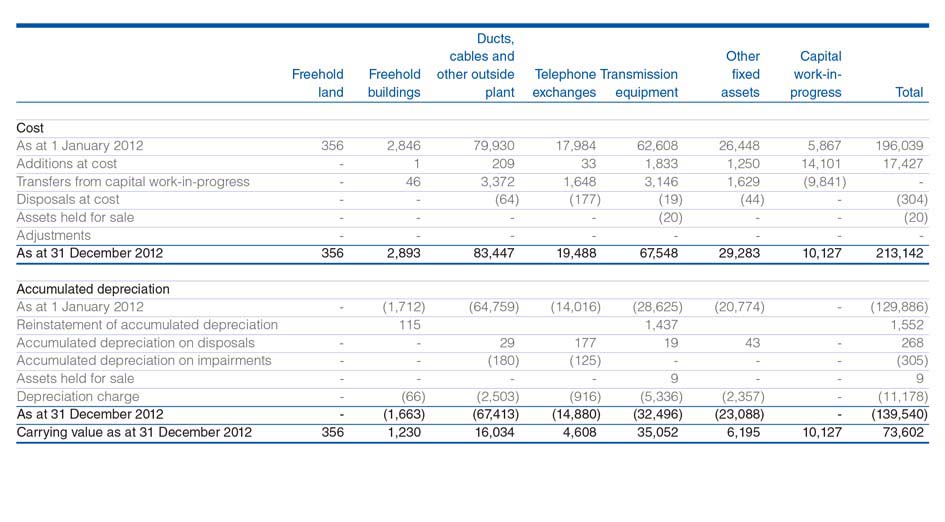

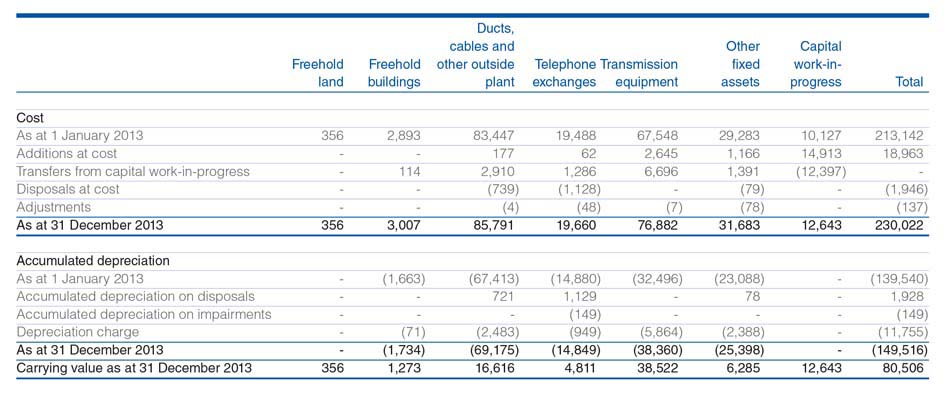

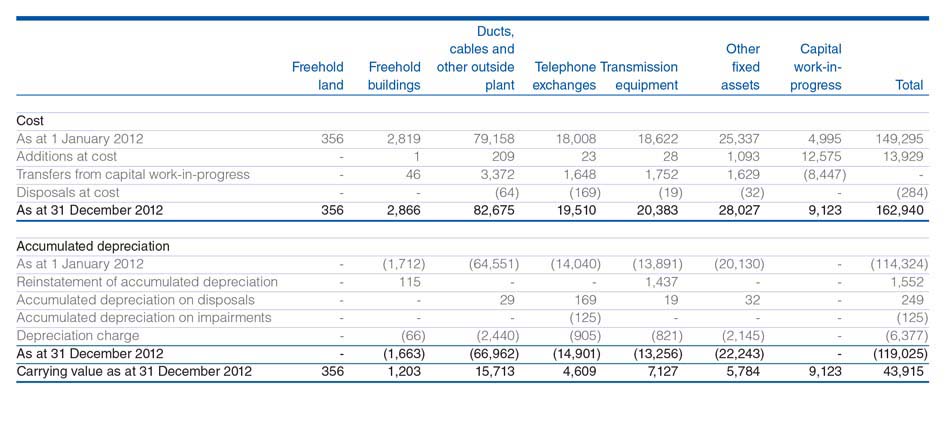

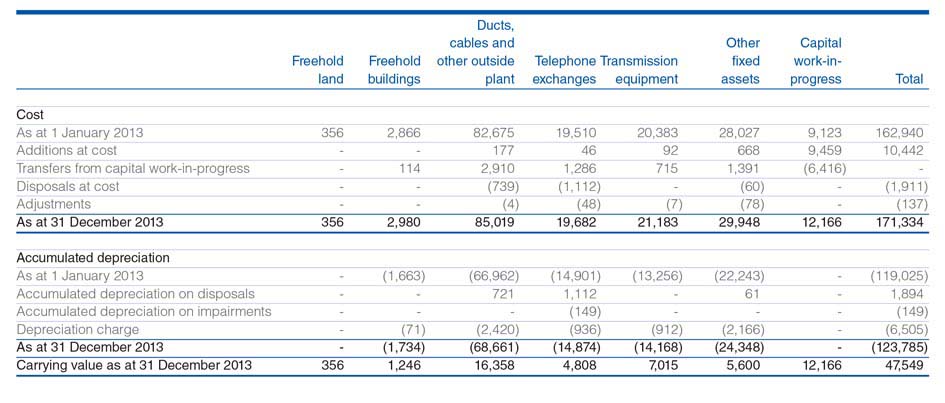

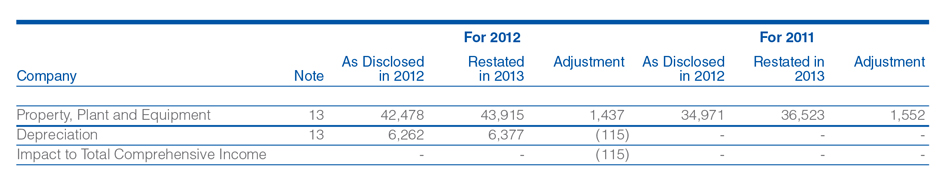

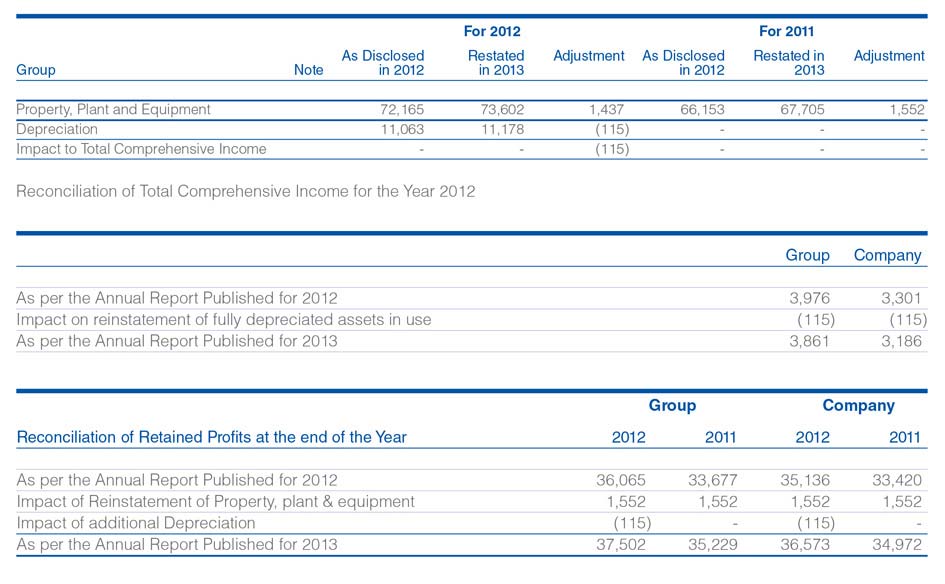

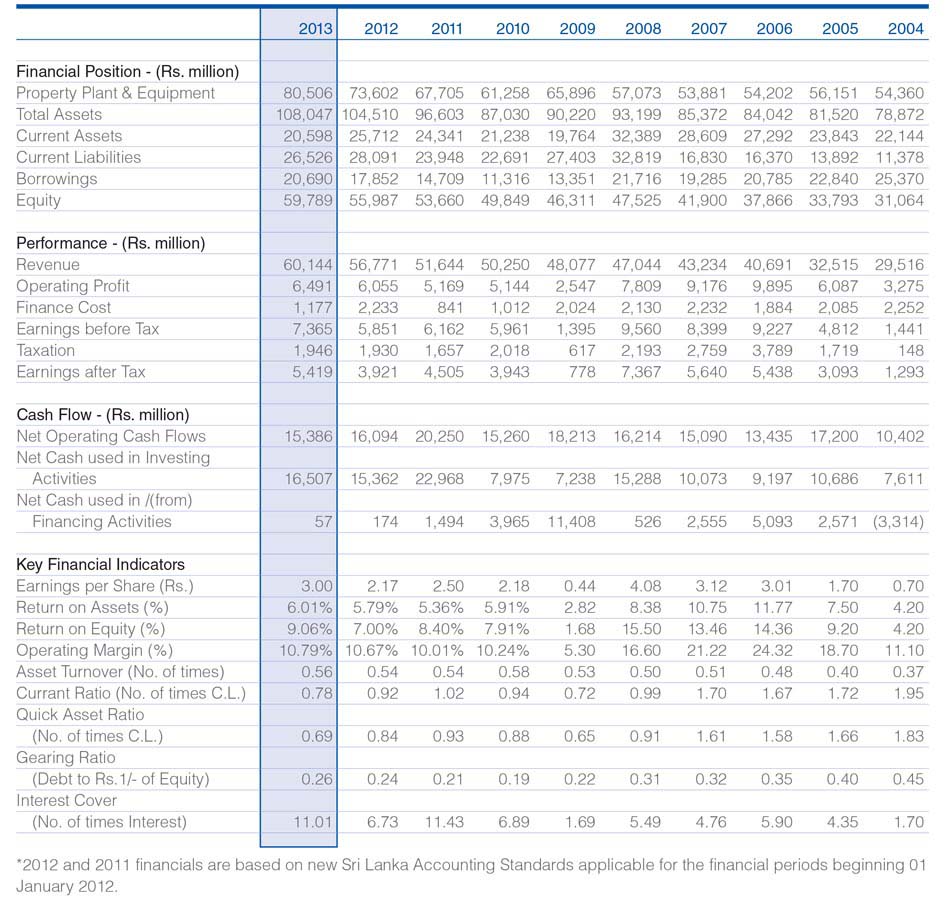

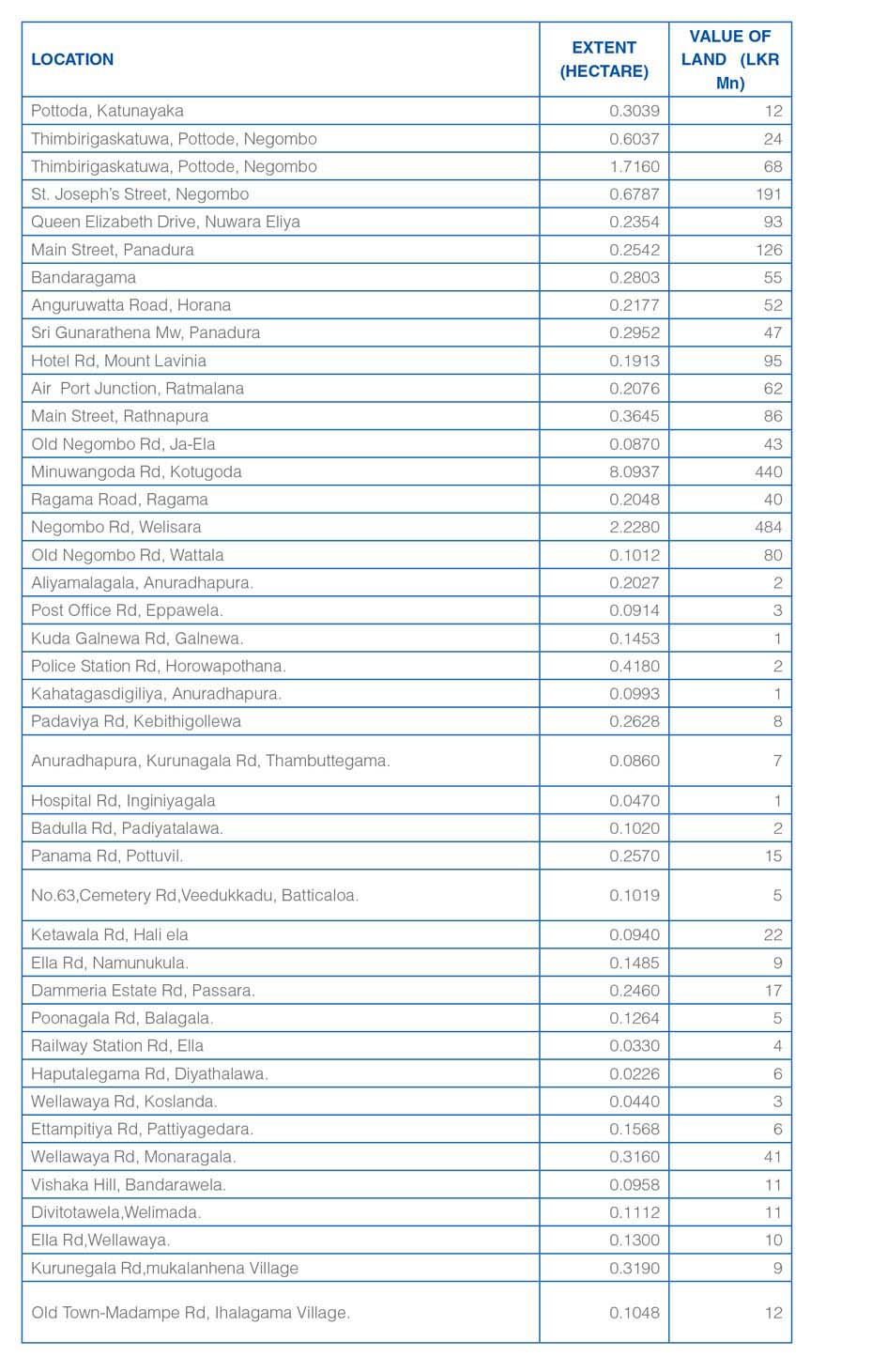

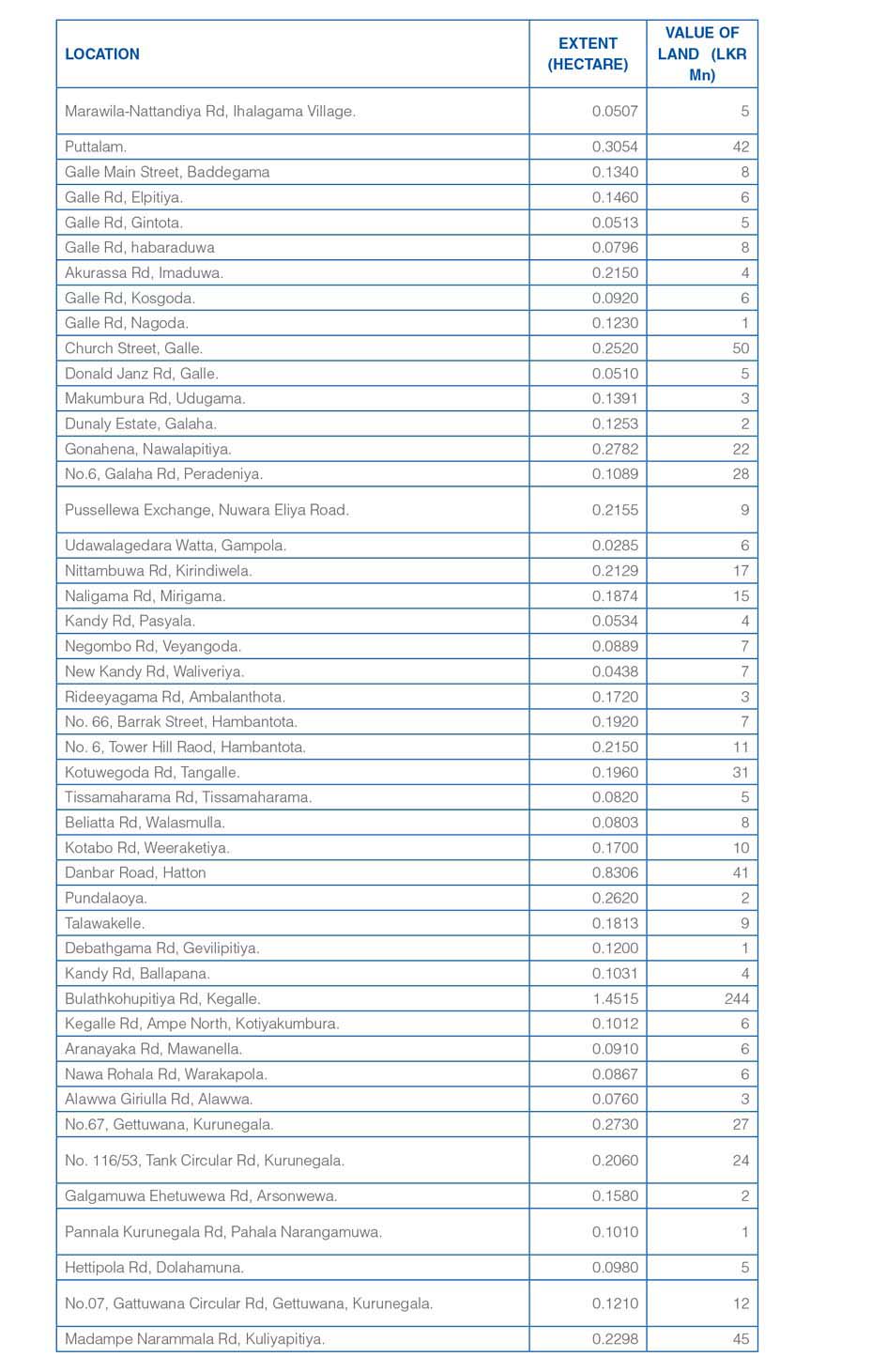

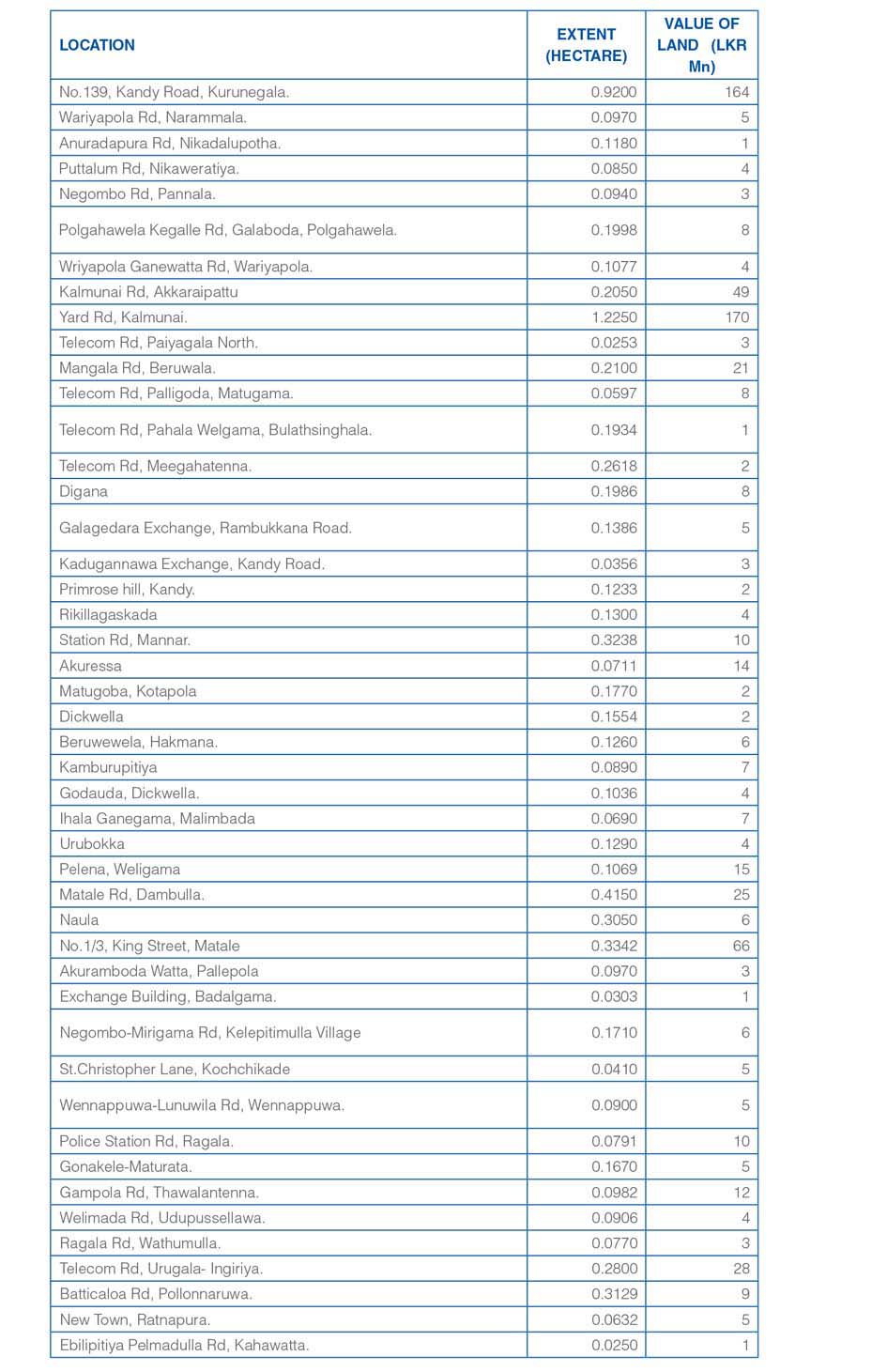

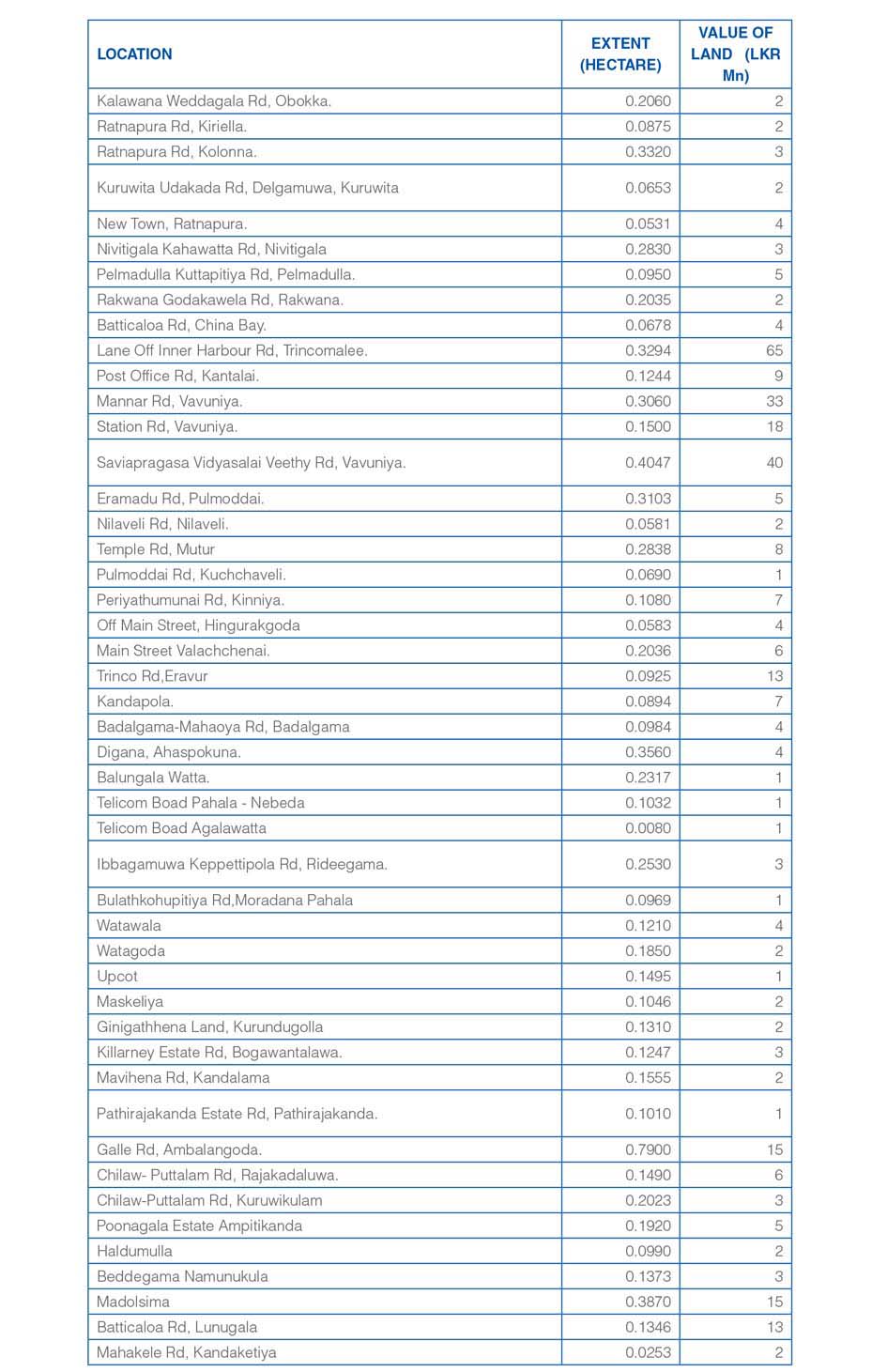

13 PROPERTY, PLANT AND EQUIPMENT

Group

Company

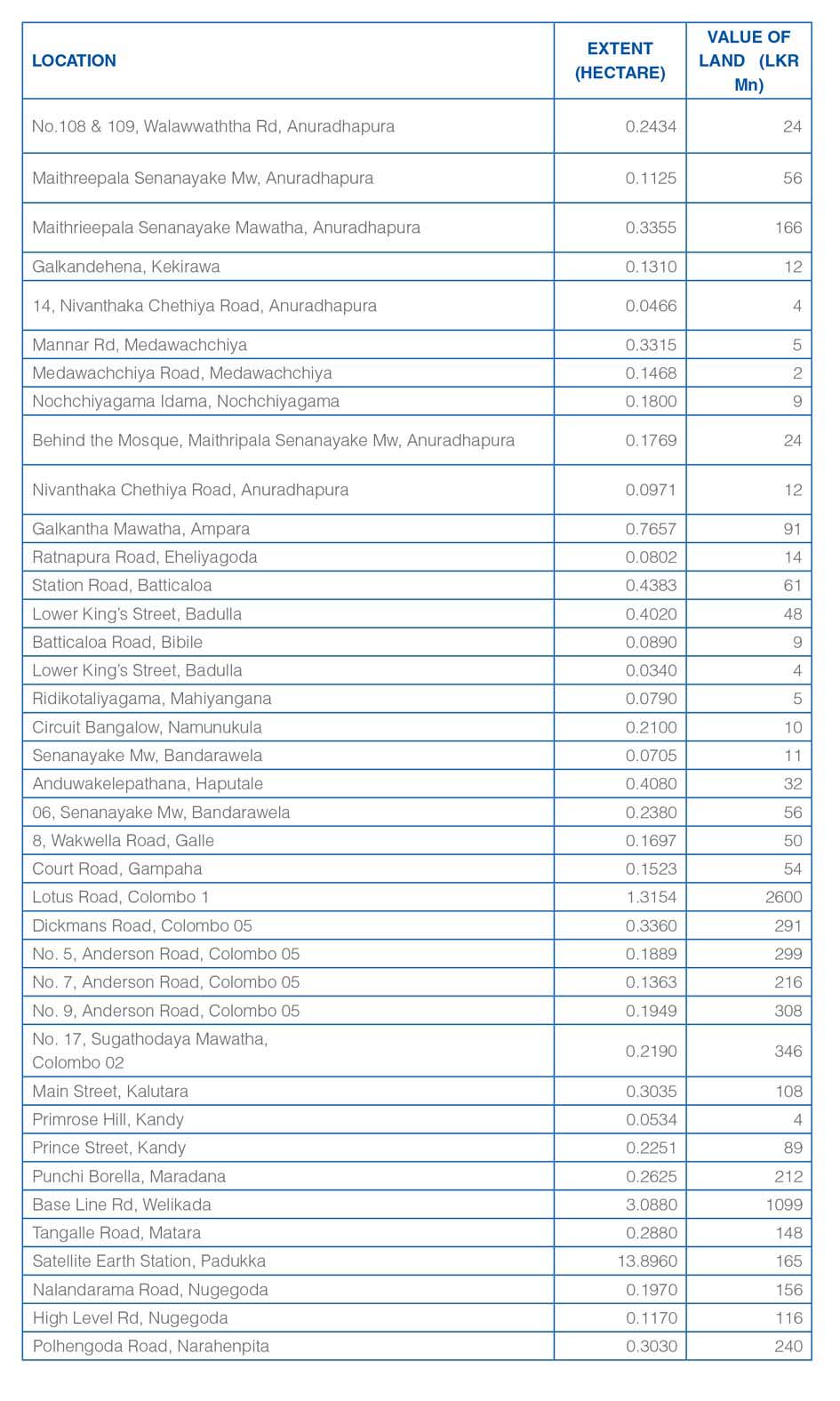

(a) On 1 September 1991, the Department of Telecommunications (DoT) transferred its entire telecommunication business and related assets and liabilities to SLT. A valuation of the assets and liabilities transferred to SLT was performed by the Government of Sri Lanka. The net amount of those assets and liabilities represents SLT’s Contributed Capital on incorporation, and the value of property, plant and equipment as determined by the Government of Sri Lanka valuers was used as the opening cost of fixed assets on 1 September 1991 in the first statutory accounts of SLT. Further, SLT was converted into a public limited company, Sri Lanka Telecom Limited (SLTL), on 25 September 1996 and on that date, all of the business and the related assets and liabilities of SLT were transferred to SLTL as part of the privatisation process.

(b) The cost of fully depreciated assets still in use in the company as at 31 December 2013 was Rs 90,907 million (2012 - Rs 83,946 million). The cost of fully depreciated assets still in use in the Group as at 31 December 2013 was Rs 94,316 million (2012 - Rs 84,603 million).

(c) No assets have been mortgaged or pledged as security for borrowings of the Company. However, Mobitel (Private) Limited, a subsidiary of the Company, has pledged its assets at a value of Rs 9.7. billion as at 31 December 2013 (2012 - Rs. 9.7 billion) for its bank borrowings [Note 22 (k)].

(d) The Directors believe that the Company has freehold title to the land and buildings transferred on incorporation (conversion of SLT into a public limited company on 25 September 1996), although the vesting orders specifying all the demarcations and extents of such land and buildings could not be traced. The Company has initiated action to transfer legal title documentations.

(e) The property, plant and equipment is not insured except for buildings & equipment situated at SLT headquarters and Welikada premises. Further, all the motor vehicles have been insured. An insurance reserve has been created together with a sinking fund investment to meet any potential losses with regard to uninsured property, plant and equipment. At the reporting date, the insurance reserve amounted to Rs 500 million (2012 - Rs 435 million) (Note 27).

(f) Impairment of assets mainly consist of the carrying value of switches Rs 149 million that were impaired as a result of implementation of Next Generation Network (NGN) ( 2012 - Rs. 125 million).

(g) Additions include assets costing Rs 224 million (2012 - Rs - nil) obtained under finance leases (where the Company is the lessee) and the additions of the Group includes assets costing Rs 249 million obtained under finance leases (2012 - Rs - nil) where the Group is the lessee.

(h) The property, plant and equipment includes motor vehicles acquired under finance leases, the net book value of which is made up as follows:

(i) Property, plant and equipment include submarine cables which are jointly controlled. The total cost and accumulated depreciation of all cables under this category are as follows;

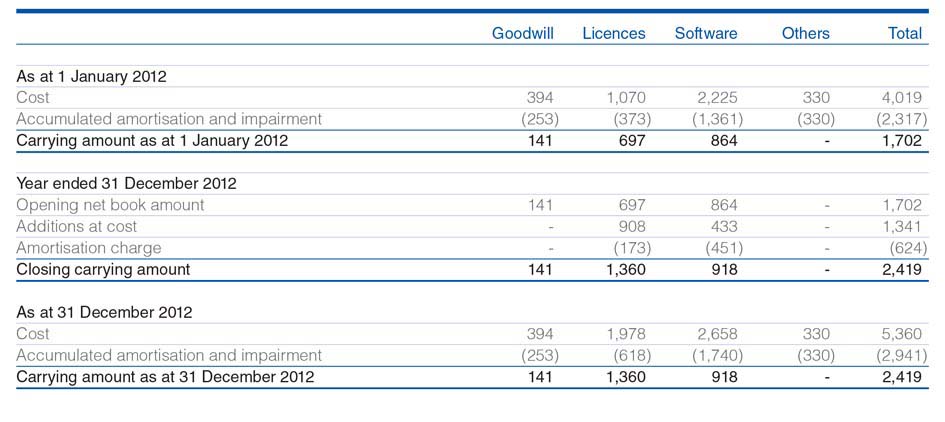

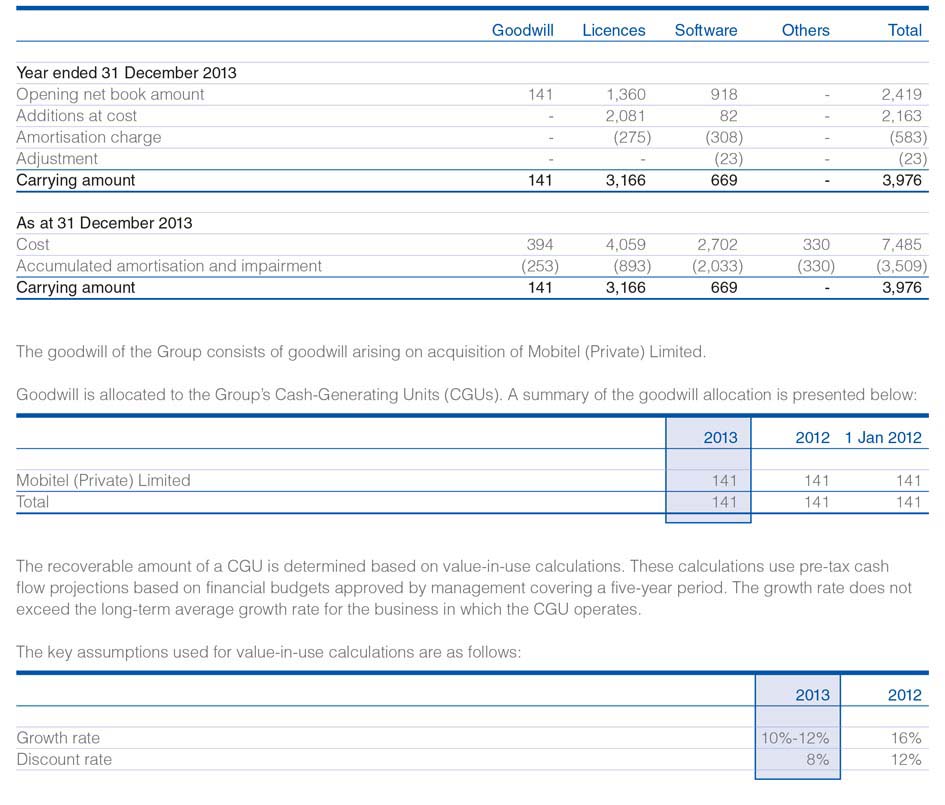

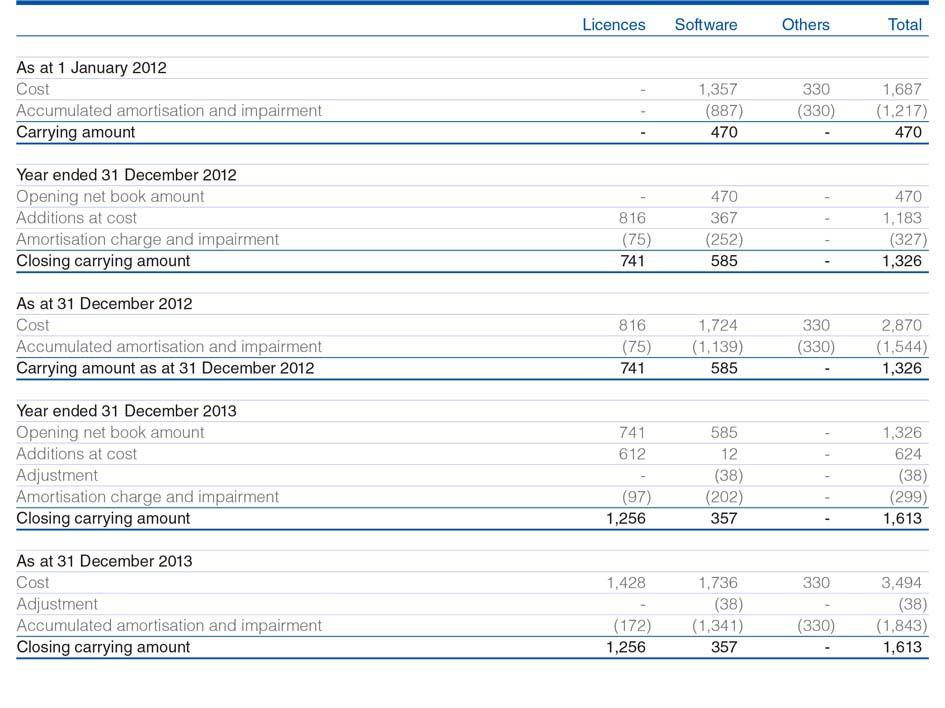

14 INTANGIBLE ASSETS

Group

Management determined budgeted gross margin based on past performance and its expectations of market development. The weighted average growth rates used are consistent with the forecasts included in industry reports. The discount rates used are pre-tax and reflect specific risks relating to the relevant operating segments. No impairment charge has been recognized for the year ended 31 December 2013 for the above CGU (2012 - Rs Nil).

Company

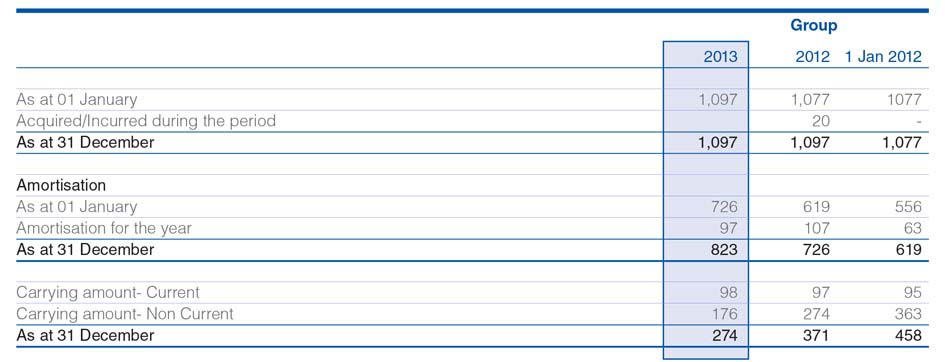

15 FINANCIAL PREPAYMENTS

Financial charges for the guarantee issued by The Swedish Export Credit Guarantee Board (EKN) for SCB loan, insurance premium for the guarantee issued by China Export and Credit Insurance Corporation for HSBC loan and other financial prepayments.

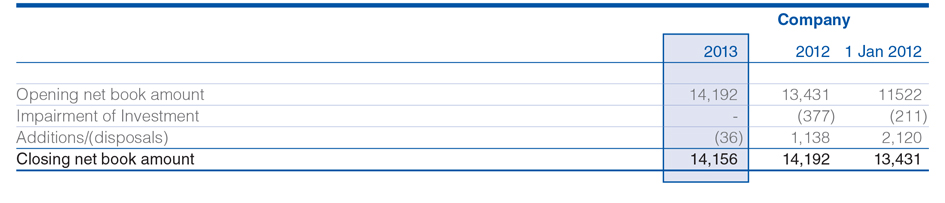

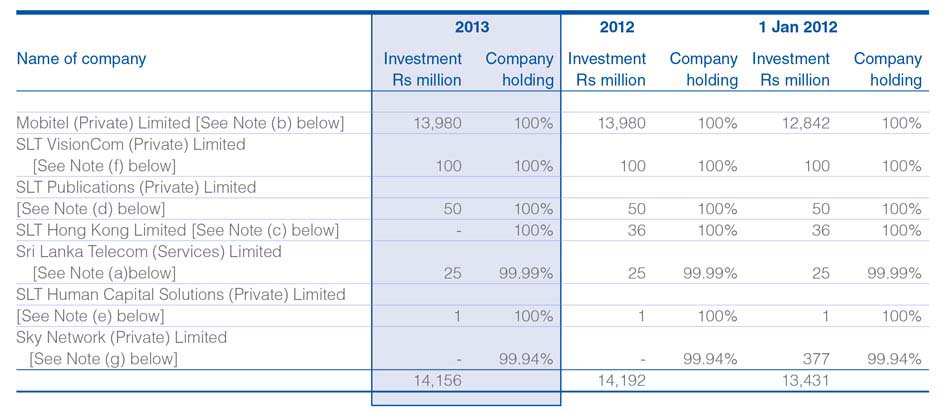

16 INVESTMENTS IN SUBSIDIARIES

Details of the subsidiary companies in which the Company had control as at 31 December are set out below:

The directors believe that the fair value of each of the companies listed above do not differ significantly from their book values.

(a) This investment in subsidiary company consists of 2,500,000 shares representing 99.99 % of stated capital of Sri Lanka Telecom (Services) Limited.

(b) The Company owns 1,320,013,240 shares representing 100% of the entire Ordinary Share capital of Mobitel (Private) Limited. At 31 December 2013.

At 31 December 2013, preference dividends amounting to Rs 980 million were in arrears (2012 - Rs 980 million). No accrual has been made in the Company’s financial statements as the Board of Directors has decided to waive off the right to receive the same.

(c) SLT Hong Kong Limited incorporated in Hong Kong is under the liquidation process.

(d) This investment in subsidiary company consists of 5,000,000 shares representing the entire stated capital of SLT Publications (Private) Limited.

(e) This investment in subsidiary company consists of 50,000 shares representing the entire stated capital of SLT Human Capital Solutions (Private) Limited

(f) This investment in subsidiary company consists of 10,000,000 shares representing the entire stated capital of SLT VisionCom (Private) Limited.

(g) This investment in subsidiary company consists of 42,071,251 shares representing a 99.94% holding of the issued stated capital and 6,000,000 12% cumulative and redeemable preference shares of Sky Network (Private) Limited.

As at 31 December 2013, preference dividends amounting to Rs 37 million (2012 - Rs 30 million) has not been recognized in the financial statements.

All the subsidiaries except Mobitel (Private) Limited and SLT Hong Kong Limited are audited by KPMG .

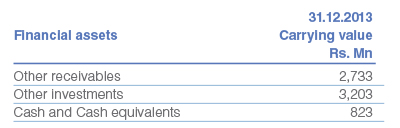

17 OTHER INVESTMENTS

Non Current Investments

Current Investments

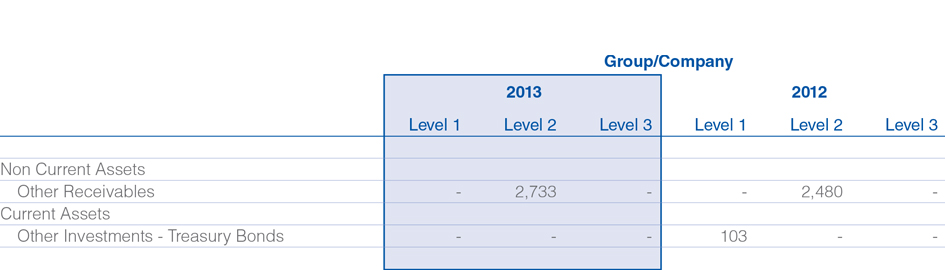

All government securities are classified as available for sale and measured at fair value and fixed deposits are classified as loans and receivables and measured at amortised cost.

Treasury bond with a carrying value of Rs. 103 Mn in 2012 which got matured during 2013 and Fixed deposits with a carrying value of Rs. 515 mn (2012 Rs. 342 mn) are restricted at bank.

Fixed Deposits with a carrying value of Rs. 3,203 includes both LKR and USD deposits.

Interest rates of other investments classified as non currents assets are as follows:

The Group provides loans to employees at concessionary rates. These employee loans are fair valued at initial recognition using level 2 inputs. The fair value of the employee loans are determined by discounting expected future cash flows using market related rates for the similar loans.

The difference between the cost and fair value of employee loans is recognized as prepaid staff cost.

The employee loans are classified as loans and receivable and subsequently measured at amortized cost.

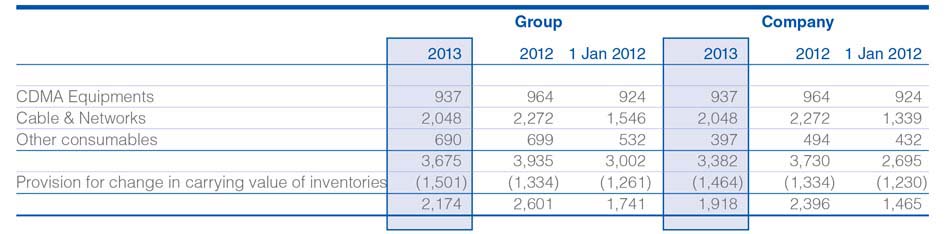

19 INVENTORIES

(a) Inventories consist of trading and capital inventory of which include telecommunication hardware, CDMA handsets, consumables and office stationery. Inventory is stated net of provisions for slow-moving and obsolete items.

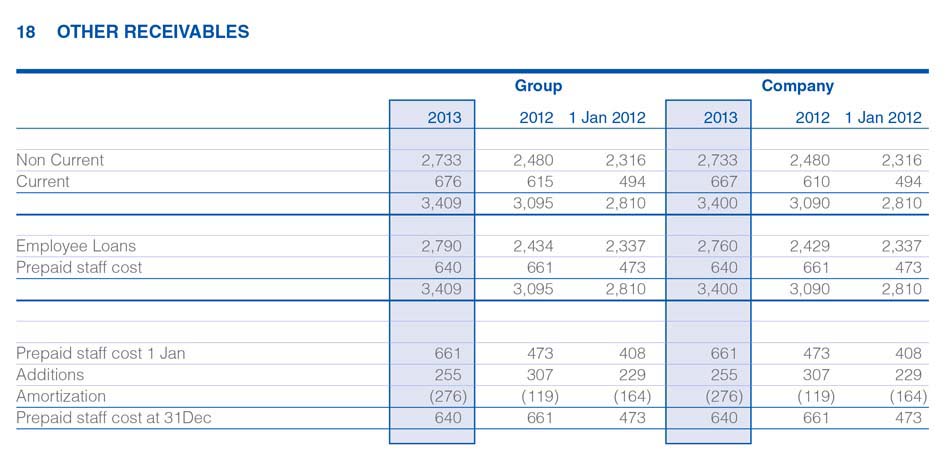

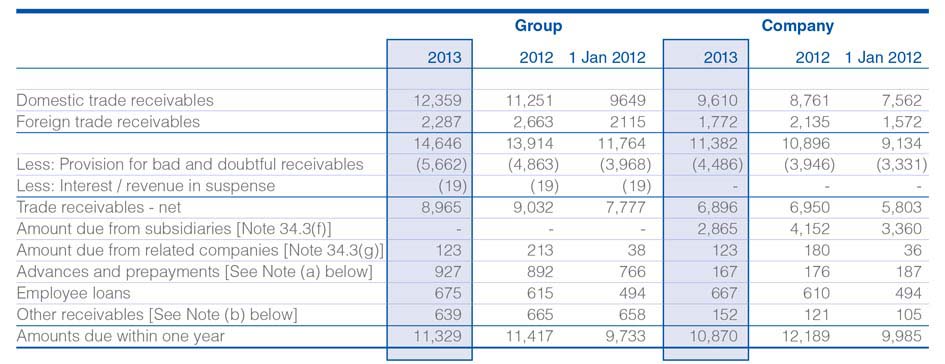

20 TRADE AND OTHER RECEIVABLES

(a) Advances and prepayments of the Company mainly consist of advances on Building rent of Rs 11 million (2012 - Rs 12 million), payments for software maintenance of Rs 120 million (2012 - Rs 120 million) and Purchase advance of Rs 4 million ( 2012-Rs 15 million.) Advances and prepayments of the Group mainly consist of advances on Building rent purchases of Rs 127 million (2012 - Rs 129 million) and payments for software maintenance of Rs 120 million (2012 - Rs 352 million) and prepayment for advertising hoardings Rs 15 million (2012- 15 million) Prepaid TRC Frequency Rs 191 mn (2012-Rs 188 million) and current portion of financial prepayment Rs 97 million (2012- Rs 97 million)

(b) Other receivables of the Company consist of refundable deposits of Rs 98 million (2012 - Rs 98 million) and dishonoured cheques of Rs 3 million (2012 - Rs 3 million). Other receivables of the Group mainly consist of refundable deposits of Rs 190 million (2012- Rs 179 million),receivables from sales agents Rs 105 million (2012-Rs 85 million ) site rentals receivables from other operators Rs 315 million (2012-Rs 304 million)

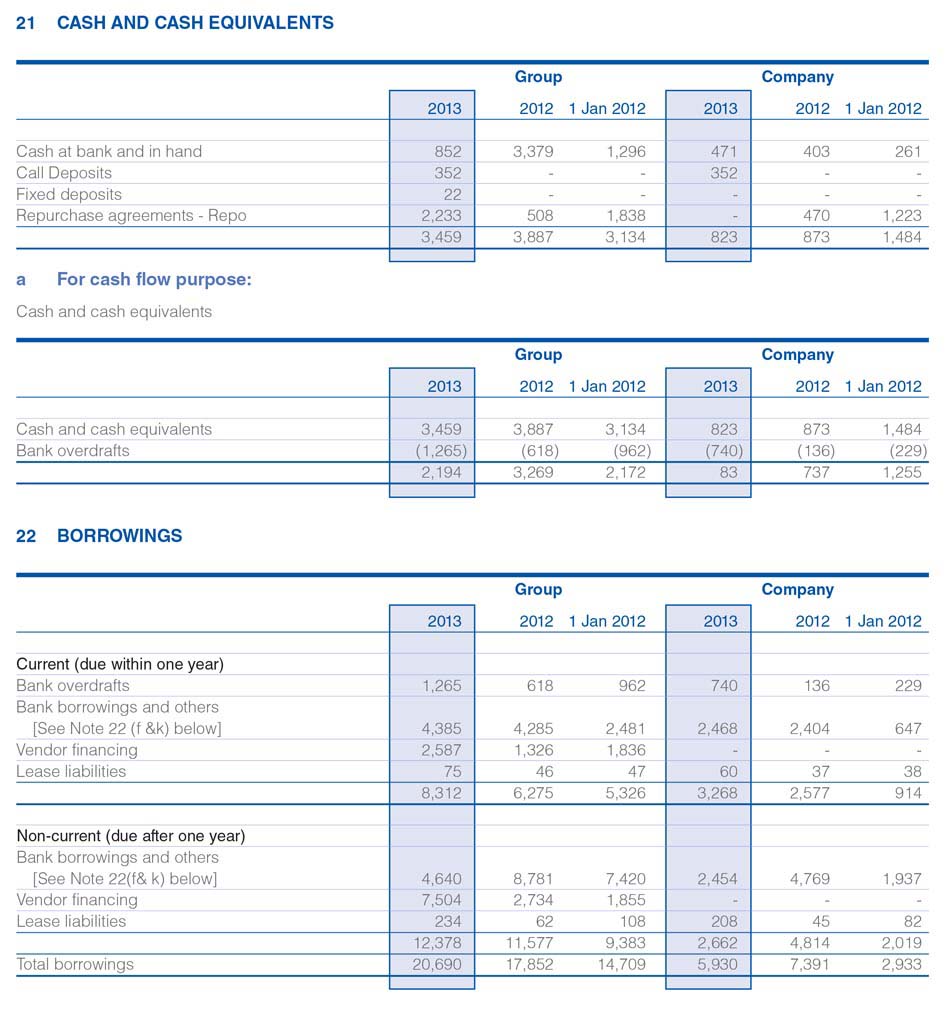

21 CASH AND CASH EQUIVALENTS

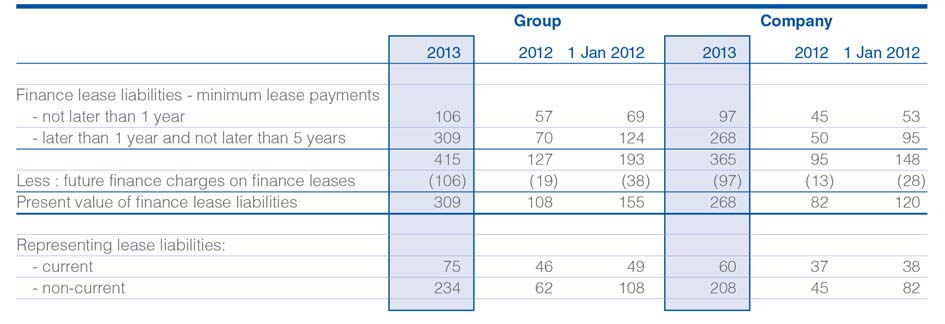

(e) Analysis of the finance lease liabilities of the Company and the Group is as follows:

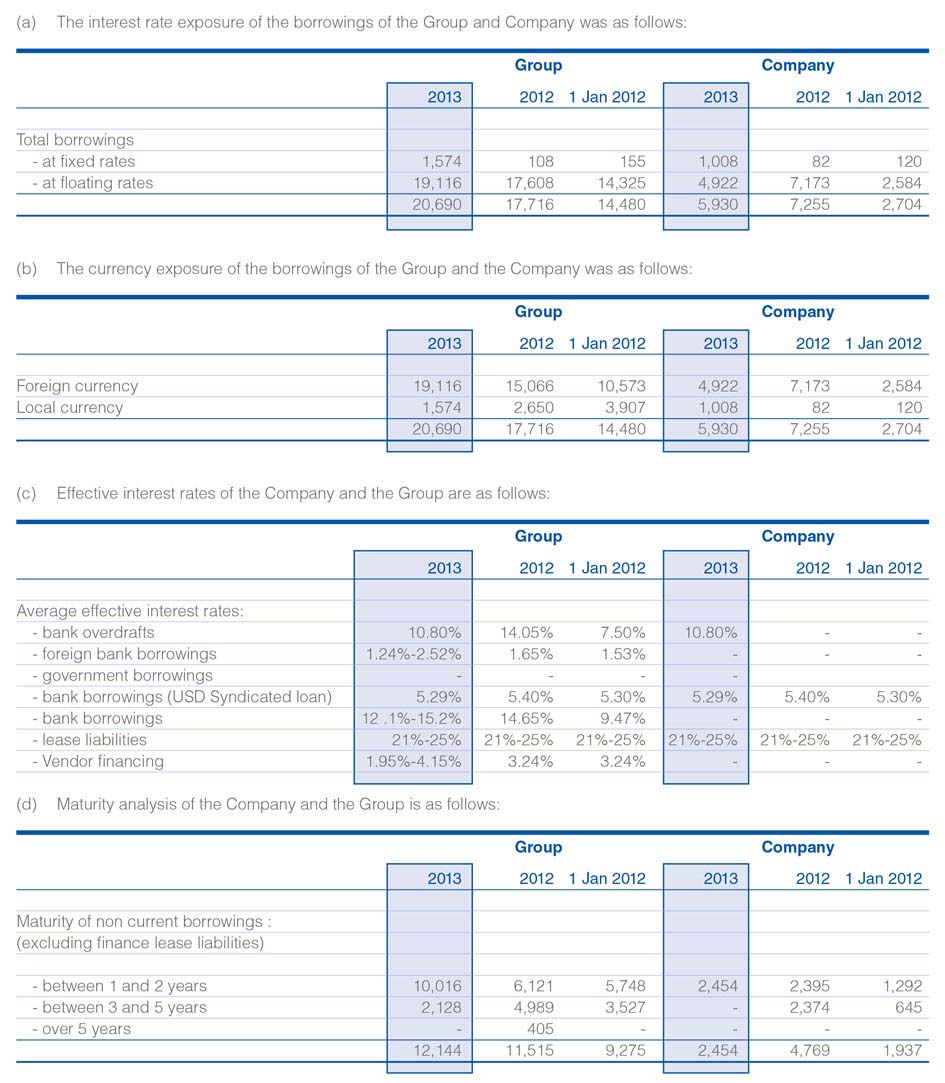

(f) Outstanding balance of USD 75 million syndicate loan as at 31 December 2013 was USD 37.5 million (LKR 4,922 million).

(g) The loan covenants include submission of audited financial statements to the lenders within specified periods from the financial year end, and to maintain adequate accounting records in accordance with generally accepted accounting principles.

(h) The Directors believe that the Company and the Group will have sufficient funds available to meet its present loan commitments.

(i) Lease liabilities of the Company and the Group are effectively secured by the lessor against the rights to the title of the asset.

(j) Bank borrowings and bank overdrafts of Mobitel (Private) Limited, a subsidiary of the Company, are secured, inter alia, by corporate guarantees given by the Company.

(k) Bank borrowings of Mobitel (Private) Limited are secured by a pledge over its property, plant and equipment at a value of Rs 9.7 billion [See Note 13 (c)]

(l) Mobitel (Private ) Limited has borrowed Rs 7,220 million during the year for the purpose of Capital expansion projects.

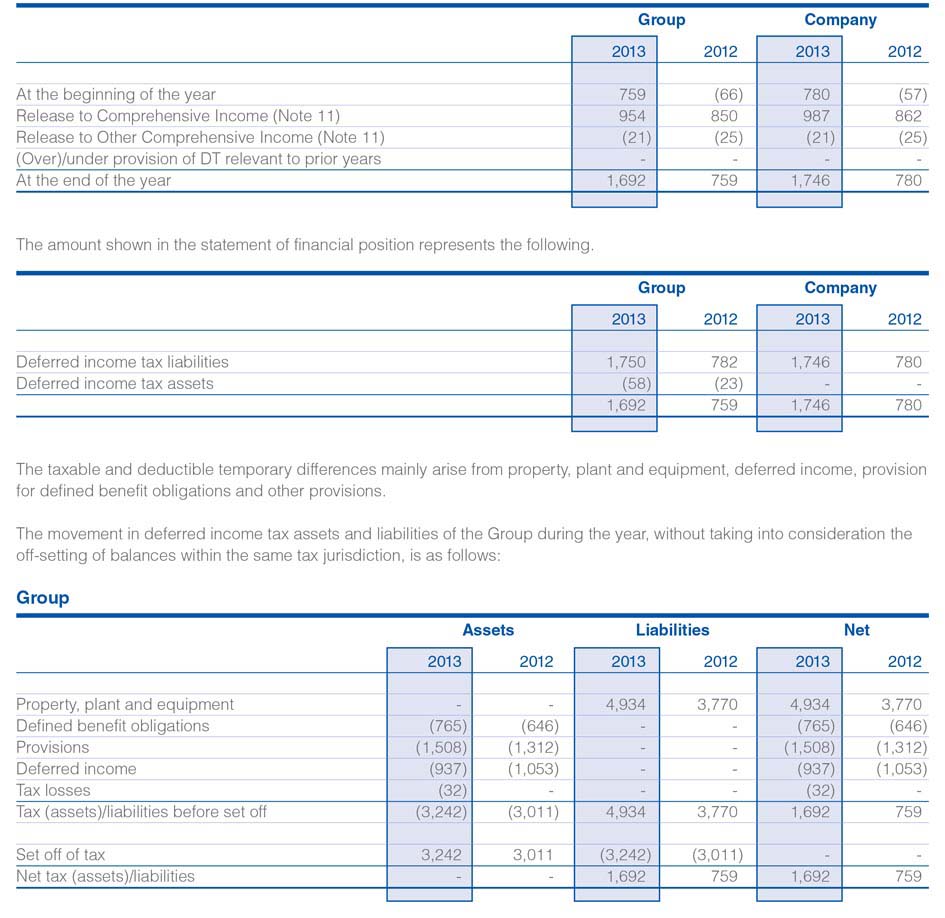

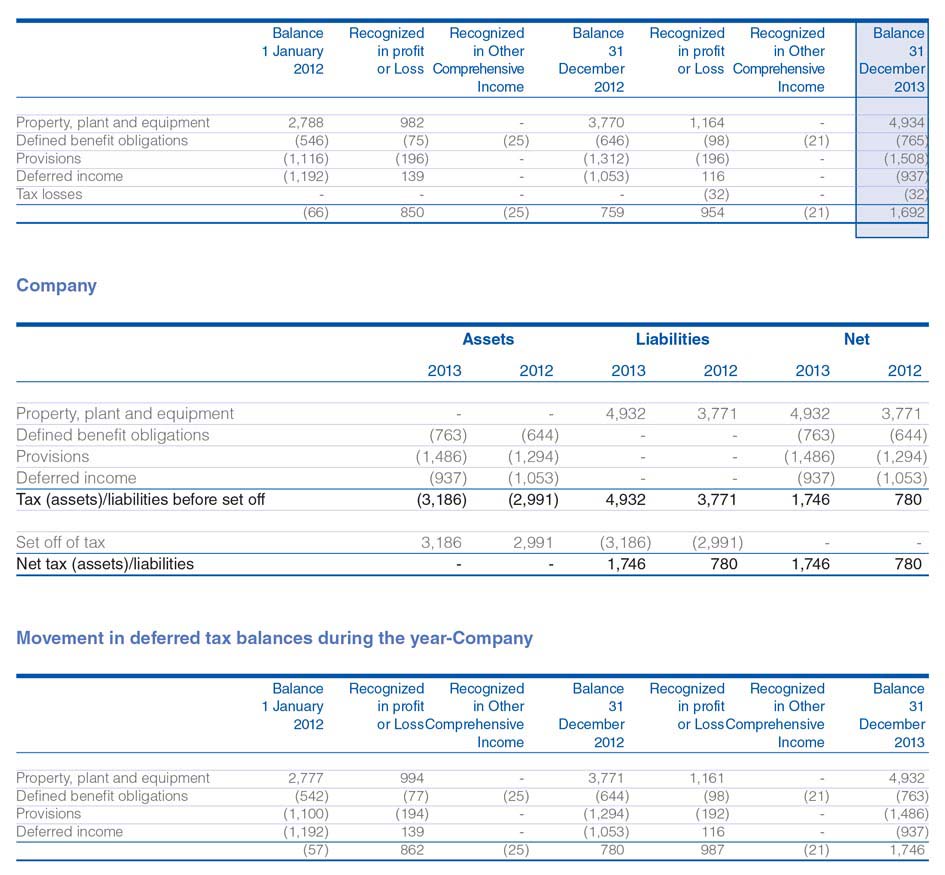

23 DEFERRED INCOME TAX

Recognized deferred income tax (assets) / liabilities

Deferred income tax (assets) and liabilities are calculated on all taxable and deductible temporary differences arising from differences between accounting bases and tax bases of assets and liabilities. Deferred income tax is provided under the liability method using a principal tax rate of 28% (for the year 2012 - 28%).

The movement in the deferred income tax account is as follows:

Movement in deferred tax balances during the year-Group

Unrecognised deferred income tax (assets) and liabilities

Deferred income tax assets are recognized for tax losses carry-forward to the extent that the realisation of the related tax benefit through future taxable profits is probable. Deferred Tax assets have not been recognized in respect of these items because it is not probable that future taxable profit will be available against which the group can utilize the benefit there from. The Group did not recognise deferred tax assets in respect of tax losses of subsidiaries amounting to Rs 200 million (2012 - 207 million) that can be carried forward to set off against future taxable income.

The adjusted tax losses available to carry forward as at 31 December 2013 are as follows:

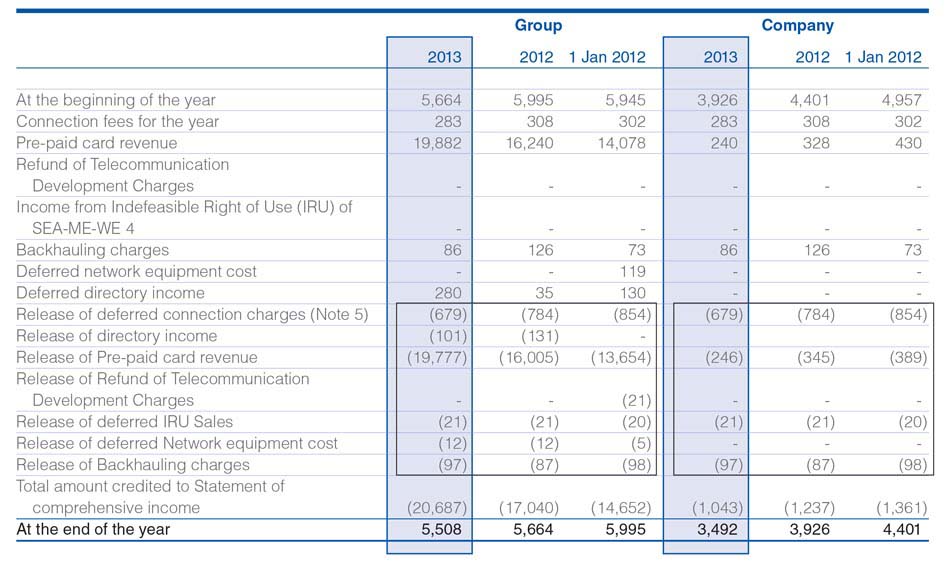

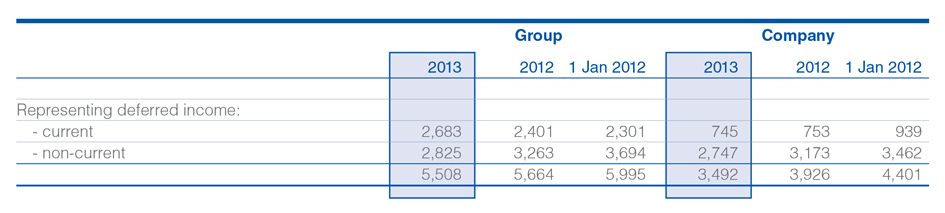

24 DEFERRED INCOME

Deferred connection charges of the Company represents the connection charges relating to PSTN network, net of amounts amortised to the Statement of comprehensive income. The connection charges are deferred over a period of 15 years as stated in Accounting Policy (v). The deferred IRU sales of the Company includes the revenue arising on sale of SEA-ME-WE 4 cable capacity which is recognized over the lease period of 15 years. Release of Backhauling charges represent the revenue arising from lease of SEA-ME-WE 3 cable capacity. Deferred Pre-paid card revenue in company represents un-used CDMA and SLT Passport cards. In addition, the deferred income of the Group mainly represents unused pre-paid card revenue and refund of Telecommunication Development Charges (TDC) received in 2009 from Telecommunication Regulatory Commission in connection with the cost of network rollout by Mobitel (Private) Limited.

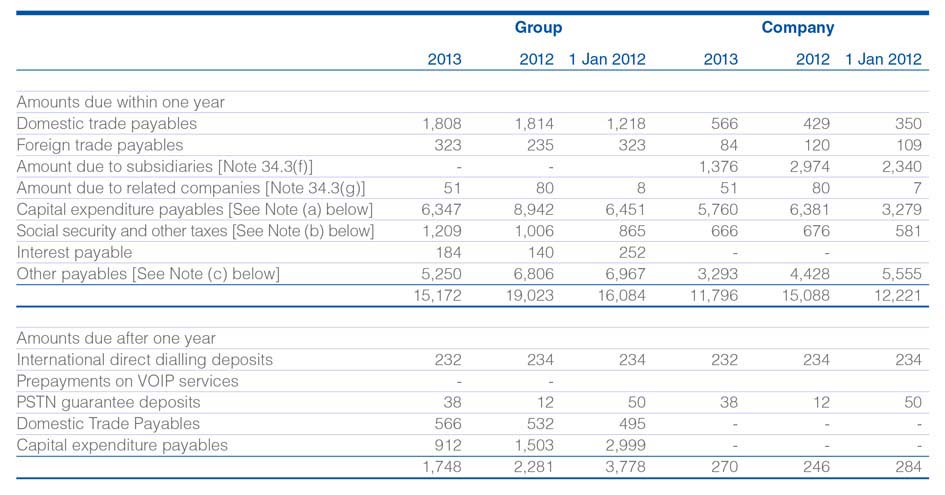

25 TRADE AND OTHER PAYABLES

(a) Capital expenditure payables of the Company mainly consist of contractors’ payable and retention of Rs 5,010 million (2012 - Rs 5,704 million) and advances on network restoration after road works of Rs 901 million (2012- Rs 676 million). Capital expenditure payables of the Group mainly consist of contractors’ payable of Rs 5,318 million (2012 - Rs 8,237 million) and advances on network restoration after road works of Rs 901 million (2012 - Rs 676 million).

(b) Social security and other taxes of the Company mainly consist of and Telecommunication Levy (TL) of Rs 344 million (2012 - Rs 379 million), Cess Rs 63 million ( 2012-Rs 59 million ), IDD Levy of Rs 18 million (2012-Rs 40 million ), EPF payable of Rs 90 million (2012 - Rs 80 million). Social security and other taxes of the Group mainly consist of Telecommunication Levy (TL) of Rs 714 million (2012- Rs 712 million ), Cess of Rs 116 million (2012 - Rs 112 million). IDD Levy payable of Rs 38 million (2012- Rs 64 million)

(c) Other payables of the Company mainly consist of dividend payable to the Government of Sri Lanka of Rs 244 million (2012 - Rs 244 million), payable for unpaid supplies of Rs 983 million (2012 - Rs 2,281 million), International Telecommunication Operators’ Levy payable of Rs 227 million (2012 - Rs 305 million) and accrued expenses and other payables of Rs 1,252 million (2012 - Rs 1,021 million). Other payables of the Group mainly consist of dividend payable to the Government of Sri Lanka of Rs 244 million (2012 - Rs 244 million), payable for unpaid supplies of Rs 983 million (2012 - Rs 2,281 million), International Telecommunication Operators’ Levy payable (without netting off TDC refunds)of Rs 252 million (2012 - Rs 330 million), and accrued expenses and other payables of Rs 2,877 million (2012 - Rs 3,122 million).

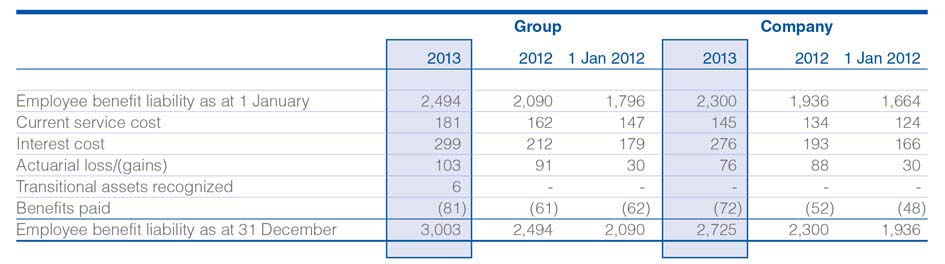

26 EMPLOYEE BENEFITS

(1) Movement in present value of employee benefit liabilities

(2) The expenses recognized in profit or loss

The expenses are recognized under staff cost in Statement of comprehensive income

(3) As stated in Accounting Policy (j) (ii) at 31 December 2013, an actuarial valuation was carried out by an independent actuary.

The principal actuarial assumptions used were as follows:

In addition to above, demographic assumptions such as mortality, withdrawal, retirement age were considered for the actuarial valuation. In 2013,1967/70 Mortality Table issued by the Institute of Actuaries London (2012 - 1967/70 Mortality Table and 2011 1967/70 Mortality Table) was taken as the base for the valuation.

The provisions for defined obligations of Sri Lanka Telecom PLC, SLT Human Capital Solutions (Private) Ltd and Mobitel (Private) Limited are actuarially valued by Messrs Actuarial and Management Consultants (Private) Limited and Piyal S Goonetilake respectively. The employee benefit liability of all other companies in the group are based on a gratuity formula based on actuarial assumption.

The provision for defined benefit obligation is not externally funded.

Sensitivity of Assumptions Employed in Actuarial Valuation

The following table demonstrates the sensitivity to a reasonably possible change in the key assumptions employed with all other variables held constant in the employment benefit liability measurement.

The sensitivity of the Statement of Comprehensive Income and Statement of Financial Position is the effect of the assumed changes in discount rate and salary increment rate on the profit or loss and employment benefit obligation for the year.

As stated in Accounting Policy 3(r) the Company transfers annually from the retained earnings an amount equal to 0.1% of additions to property, plant and equipment to an insurance reserve. An equal amount is invested in a sinking fund to meet any funding requirements for potential losses from uninsured property, plant and equipment.

Management regularly monitors the charges made against the insurance reserve and the adequacy of the provision made.

28 GRANT

(a) Grant in Company and Group consists of Exchange equipment received from Alcatel CIT France in 2005.

29 STATED CAPITAL

30 FINANCIAL RISK MANAGEMENT

Overview

The Group has exposure to the following risks from its use of financial instruments:

Credit risk

Liquidity risk

Market risk

This note presents information about the Group’s exposure to each of the above risks, the Group’s objectives, policies and processes for measuring and managing risk, and the Group’s management of capital. Further quantitative disclosures are included throughout these financial statements.

Credit Risk

Credit risk is the risk of financial loss to the Group if a customer or counter party to a financial instrument fails to meet its contractual obligation, and arise principally from the Group’s receivables from customers.

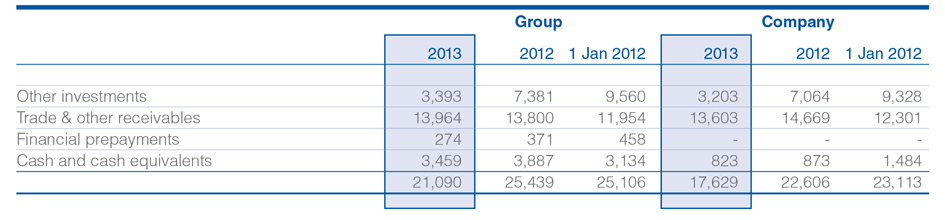

Carrying amount of financial assets represents the maximum credit exposure

The maximum exposure to credit risk at the reporting date was as follows;

Carrying value

Management of Credit risk

The group has a very well established credit policy for both International Interconnect customers and Domestic customers to minimize credit risk. A separate committee has been established to evaluate and recommend the credit worthiness of the International Interconnect customers. Further prepaid sales are used as a means of mitigating credit risk.

Domestic service is offered to a new customer only after scrutinizing the internal blacklisted data base. The group has a well-established credit control policy & process to minimize credit risk. Customers are categorized according to the segments and credit limits have been fixed as per their average monthly bill value. Customer usage and bill payments are monitored as per the credit limits. Credit limit will be periodically revised as per the past monthly bill values. High risk voice customers are subjected to automated disconnection when they reach the threshold limits. Credit control actions and recovery actions are taken for overdue customers and defaulted customers to minimize credit risk. High revenue generating customers including corporate customers are monitored individually.

Impairment losses

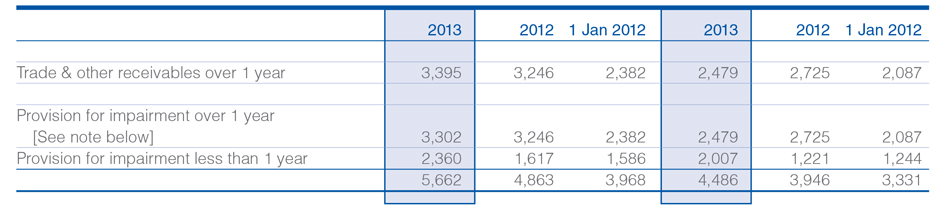

The aging of trade and other receivables at the reporting date that were impaired are as follows

Mobitel (Private) Limited, SLT Publications (Private) Limited and Sri Lanka Telecom (Services) Limited have not impaired certain trade receivables over one year amounting to Rs. 41 million, Rs. 29 million and Rs. 23 million respectively as at 31 December 2013.

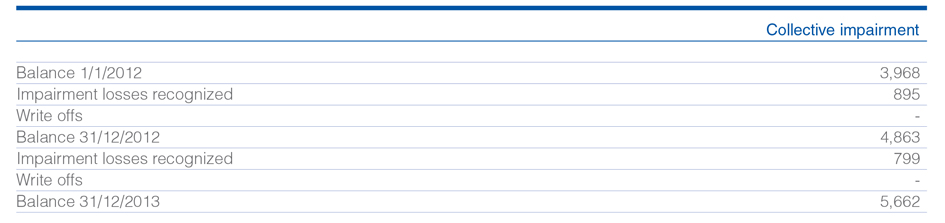

The movement in the provision for impairment in respect of trade and other receivables during the year was as follows:- Group

Other investments

The Group limits its exposure to credit risk by investing only in government debt securities, repos and in short term deposits with selected bankers with Board approval.

Guarantees

Sri Lanka Telecom PLC provides corporate guarantees to its subsidiaries only.

Liquidity Risk

Liquidity risk is the risk that the Group will encounter difficulty in meeting the obligations associated with its financial liabilities that are settled by delivering cash or another financial asset. The Group’s approach to managing liquidity is to ensure, as far as possible, that it will always have sufficient liquidity to meet its liabilities when due, under both normal and stressed conditions, without incurring unacceptable losses or risking damage to the Group’s reputation.

The group ensures its liquidity is maintained by investing in short, medium and long-term financial instruments to support operational and other funding requirements. The group determines its liquidity requirements by the use of both short and long-term cash forecasts. These forecasts are supplemented by a financial headroom analysis which is used to assess funding adequacy for at least a 12-month period and the same is reviewed on an annual basis.

Short and medium-term requirements are regularly reviewed and managed by the treasury division

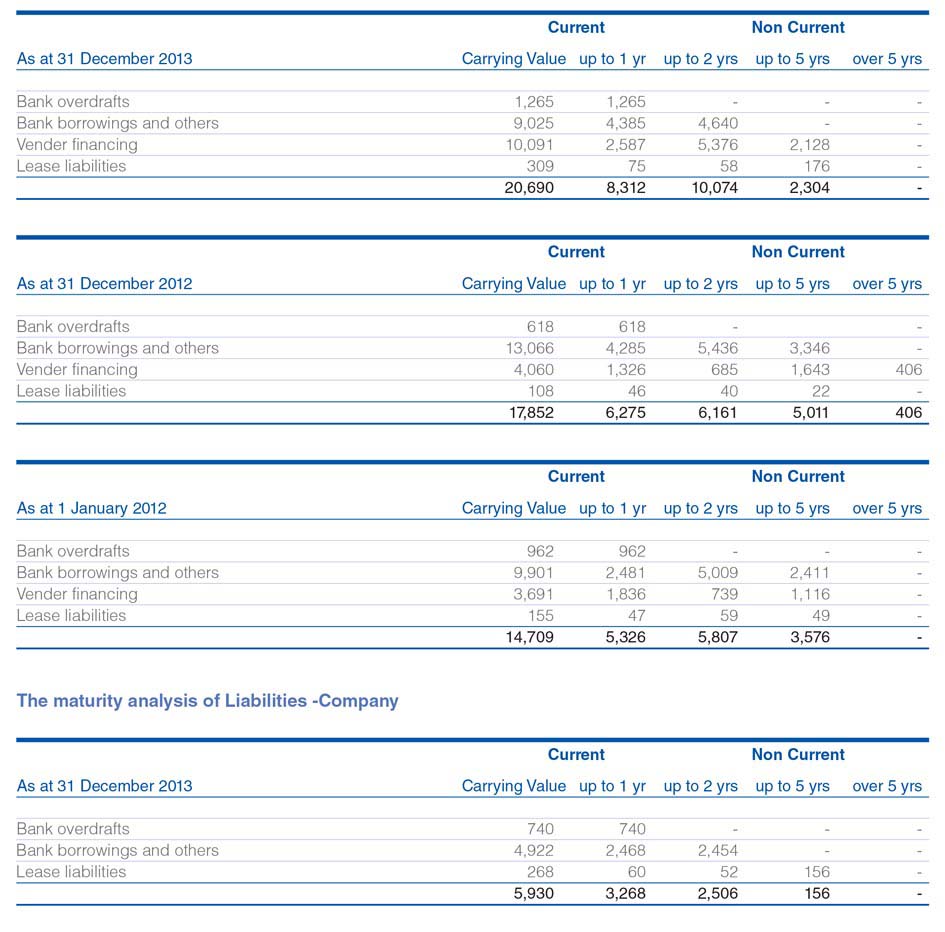

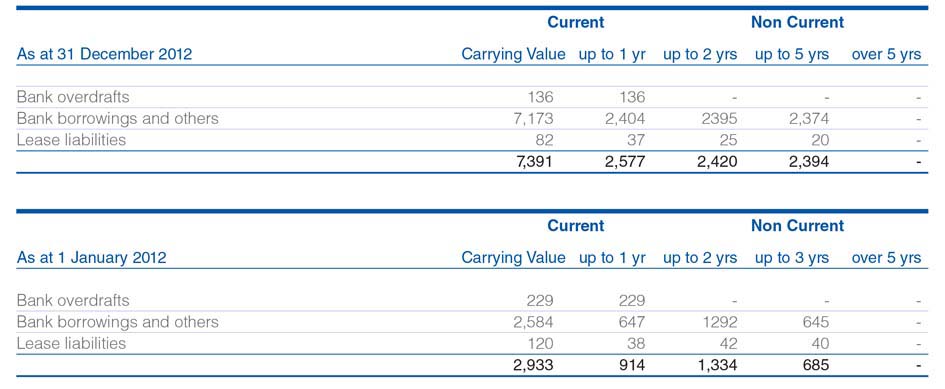

The maturity analysis of Liabilities -Group

Market Risk

Market risk is the risk that changes in market prices, such as foreign exchange rates, interest rates and equity prices which will affect the Group’s income or the value of its holdings of financial instruments. The objective of market risk management is to manage and control market risk exposures within acceptable parameters, while optimising the return.

Currency Risk

The Group is exposed to currency risk on services provided, services received and borrowings, deposits that are denominated in a currency other than the Sri Lankan rupees (LKR)

The Group manages its currency risk by a natural hedging mechanism to a certain extent by matching currency outflows for repayments of foreign currency loans and services with currency inflows for services settled in foreign currencies.

Exposure to currency risk

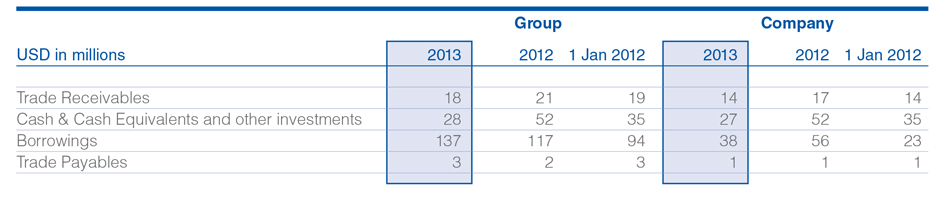

The summary of quantitative data about the Group’s exposure to foreign currency was as follows:

Interest Rate Risk

Interest rate risk mainly arises as a result of Group having interest sensitive assets and liabilities, which are directly, impacted by changes in the interest rates. The Group’s borrowings and investments are maintained in a mix of fixed and variable interest rate instruments and periodical maturity gap analysis is carried out to take timely action and to mitigate possible adverse impact due to volatility of the interest rates.

Foreign currency borrowings at variable rate of interest rate with a cap minimizes any adverse impact due to an upward movement of USD interest rate in the market

Short-term interest rate management is delegated to the treasury operations while long-term interest rate management decisions require approval from the Board of Directors

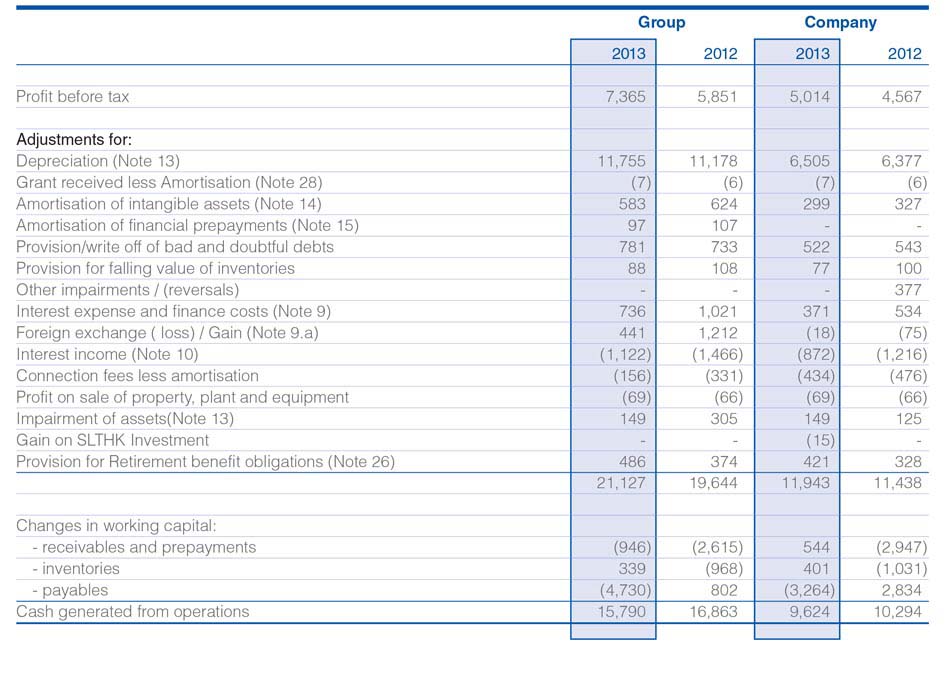

31 CASH GENERATED FROM OPERATIONS

Reconciliation of profit before tax to cash generated from operations:

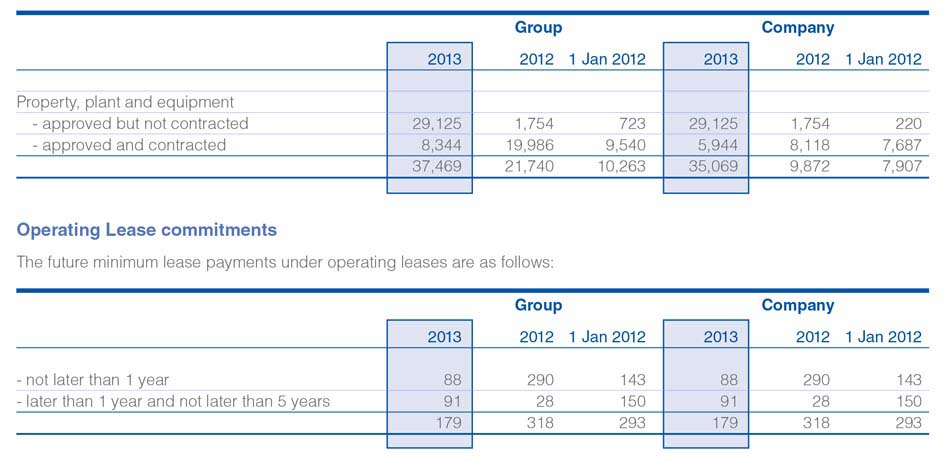

32 CAPITAL COMMITMENTS

The Group and the Company have purchased commitments in the ordinary course of business as at 31 December 2013 as follows:

Letter of Credit Commitments

Outstanding letter of Credit of the Company and Group as at 31 December 2013 amounted to Rs 949 million and Rs 1,404 million respectively.

Other financial commitments

Except for any regular maintenance contracts entered into with third parties in the normal course of business, there are no other material financial commitments that requires separate disclosure.

33 CONTINGENCIES

(a) Global Electroteks Limited has initiated legal action under High Court Case No. 20/2006 claiming damages of USD 12 million from SLT PLC for unlawful disconnection of interconnection services. The Trial is proceeding. Next date 24 February 2014

(b) SC (CHC) 31/2010 - Directories Lanka (Private) Limited (DLPL) Appeal Case filed by DLPL against SLT PLC, against the dismissal of CHC 2/2006(3) by which DLPL claimed damages of Rs. 250 mn,for alleged unfair competition with regard to artwork on the coverpage of the Directory by SLT.

The Appeal proceedings have still not commenced in the Supreme Court.

(c) Just In Time Holdings (Pvt.) Ltd (JIT) is claiming USD 4,738,846, as payments due to them from SLT under the contract with damages. Proceedings are concluded and award was delivered in favour of JIT on 30 March 2012 with damages, costs and legal interest. SLT PLC has received legal advice that it has sufficient legal grounds to challenge the arbitral award including damages ,costs and legal interest under the award.

SLT PLC is proceeding with an appeal (case no HC/ARB/141/2012)against the award delivered based on these substantial legal arguments. Next date of oral submission 28 March 2014.

(d) HC/ARB/02/2013 - Just In Time Holdings Private Limited has filed application to enforce the award of arbitration given in favour of JIT at the conclusion of the arbitration between JIT and SLT in terms of section 31 of Arbitration Act.

Next date of Oral Submissions 28 March 2014

(e) Rates & Taxes -DSP/00111/08, Application against the unreasonable increase of Assessment Tax of SLT Headquarters, to Rs. 8,452,500 per Quarter from the year 2006.

Legal action filed by SLT against Colombo Municipal Council, against the arbitrary increase of assessment value of head quarters premises from Rs. 84 million to Rs. 96 million. The quarterly assessment tax increase from 2006 was Rs 7,350,000 to Rs 8,452,500

The case is proceeding and will be called on 28 March 2014.

(f) WP/HCCA/COL/106/LA -Appeal made by Colombo Municipal Council against the stay order granted in favor of SLT PLC precluding CMC levying the aforementioned Assessment taxes from SLT PLC is pending in Court.

On 20 February 2014, counsels of both parties informed court that they have agreed to negotiate the matter further to enter into a settlement.

(g) 12/2008 CBCU, An Inquiry started by Sri Lanka Customs - A consignment of CDMA equipment were detained in October 2008 by the Customs Authority. Subsequently the equipment were cleared pending inquiry, based on a Cash deposit and Bank guarantee Submitted by SLT for the total value of Rs. 122,189,514/- . Currently under this inquiry no further date has been given to SLT to proceed with the matter.

(h) Customs Case No. ADP/031/2009 – Goods valued at USD 996,785 which was imported under the last consignment of equipment for NGN Phase II expansion project were detained by the Custom on or about 14th May 2009. Subsequently the equipment were cleared on 18.07.2009. Pending inquiry, based on a Bank Guarantee placed by SLT to the value of Rs. 35,000,000/-.

The inquiry is proceeding and a written submission was submitted to the NC committee.

NC Committee session was held on 28 January 2014 and their decision is pending.

(i) Arbitration initiated by JITHPL claiming arrears under agreement between JITHPL and SLT to provide WAN connection to NSB. SLT has a back to back agreement with NSB and NSB has failed to make payments under the agreement. SLT terminated the agreements with JIT in November 2011, upon termination of the SLT agreement with NSB. JIT is claiming Rs. 34 mn as moneys for the period upto termination, Rs. 10 mn as interest and Rs. 13 mn as rentals upto unexpired period of the case.

Hearing - 06 May 2014.

The Company has provided guarantees on behalf of its Subsidiaries for following credit and trade finance facilities.

(i) Facilities amounting to Rs 5,750 million (2012 - Rs 6,730 million) and USD 191.2 million (2012 - USD 159.4 million) for Mobitel (Private) Limited for the GSM rollout stage 3, 4, 5, 6.and 7

(ii) Facilities amounting to Rs 26 million (2012 - Rs. 26 million) for Sri Lanka Telecom (Services) Limited to obtain facilities for working Capital requirement.

(iii) With regard to cases detailed above, pending the outcome of the appeals and hearings, no provisions have been recognized in the financial statements up to 31 December 2013.